SCR Calculator User Manual

Version 1.17 Last modified 2025-4-6

Single Asset SCR Outputs

After entering all required inputs, click the "Calculate" button to display two panels:

- The "Solvency Capital Requirements" panel on the right

- The "Cashflows & Sensitivities" panel at the bottom

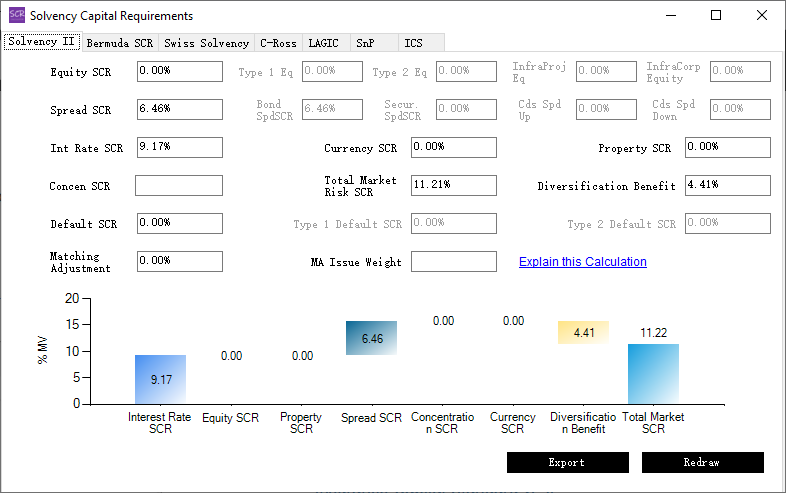

The Solvency Capital Requirements (SCR) panel is straightforward to navigate. A screenshot is provided below. Each tab corresponds to a specific regulatory regime. For additional clarity, click the "Explain this Calculation" link.

The "Redraw" button recalculates the total market SCR and diversification benefit based on the component SCR values entered in the textboxes and updates the waterfall chart. This feature is helpful for users to adjust individual component SCRs and assess their marginal impact on the total SCR. However, re-clicking the "Calculate" button in the main form will overwrite all SCR values in this panel.

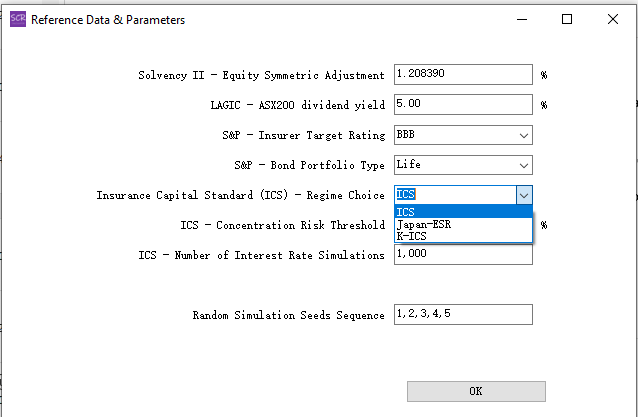

How to Access Japan-ESR and Korean-ICS

The Japan-ESR and Korean-ICS tabs are hidden by default. To access them, go to "Data & Parameters" → "Reference Data & Parameters," as shown below:

Once selected, the ICS tabs will switch to display Japan-ESR or Korean-ICS data. These are variations of the ICS regime and are grouped under the same output tab for simplicity.

Detailed Explanations

Below are explanations of the textboxes in each of the SCR tabs:

"Solvency II" tabEquity SCREquity Solvency Capital Requirement - an aggregated value from the next four entries.Type 1 EquityMainly Developed Market Traded Equities; also some special PE funds.Type 2 EquityEmerging Market equities, Hedge Funds and most Private Equities.Infra ProjectInfrastructure Project equity, a special type under Solvency II that enjoys some capital relief.Infra CorpInfrastructure Corporate equity, also enjoys some capital relief compared to normal equities, but less so than Infrastructure Project equity.Spread SCRSpread Solvency Capital Requirement - an aggregated value from the next four entries.Spread BondSpread SCR from credit bonds.Spread SecurSpread SCR from securitised positions.Spd Deri UpSpread SCR from Credit Derivatives under the spread-up shock. Only one of spread-up and spread-down shocks is used.Spd Deri DownSpread SCR from Credit Derivatives under the spread-down shock. Only one of spread-up and spread-down shocks is used.Interest Rate SCRInterest rate SCR from all fixed income assets under the interest rate up/down scenarios. Only one of rate-up and rate-down shocks is used.Currency SCRCurrency solvency capital requirement.Property SCRProperty solvency capital requirement.Concentration Risk SCRConcentration risk solvency capital requirement. Normally only calculated at total B/S level.Total Market Risk SCRTotal market risk SCR - an aggregate of equity, property, spread, interest rate, concentration and currency risks.Diversification BenefitDiversification Benefit - the difference between the arithmetic sum of the individual risk capital and the total market risk SCR.Counterparty Default SCRCounterparty Default SCR - an aggregated value from the next two entries.Type 1 Default SCRType 1 Counterparty Default Risk SCR.Type 2 Default SCRType 2 Counterparty Default Risk SCR.Probability of DefaultThe annual probability of default series for the bond over its lifespan, starting from the nearest year. Presented for each year of the life of the bond. These probabilities can be used to de-risk the cashflows in the case of annuity cashflows. These values have been interpolated for each point in time, using EIOPA or PRA published data. Where PRA data is used and relevant, the notch-level interpolation method is also used.Probability of Default (bps)Probability of default in the form of bps that represents a proportion of the bond's Z-spread. Presented for each year of the life of the bond. These values have been interpolated for each point in time, using EIOPA or PRA published data. Where PRA data is used and relevant, the notch-level interpolation method is also used.Cost of Downgrade (bps)Cost of Downgrade in the form of bps that presents a proportion of the bond's Z-spread. Presented for each year of the life of the bond. These values have been interpolated for each point in time, using EIOPA or PRA published data. Where PRA data is used and relevant, the notch-level interpolation method is also used.Long-Term Aver. Spread (bps)Long-Term Average Spread in the form of bps that were calibrated using historical data. Presented for each year of the life of the bond. These values have been interpolated for each point in time, using EIOPA or PRA published data. Where PRA data is used and relevant, the notch-level interpolation method is also used.Fundamental Spd (bps)Calculated based on regulatory formula and using PD, CoD and LT Average Spread as input parameters. Calibrated for each year of the life of the bond. These values have been interpolated for each point in time, using EIOPA or PRA published data. Where PRA data is used and relevant, the notch-level interpolation method is also used.MA Potential (bps)Matching Adjustment calculated as the spread-over-RFR (i.e. Z-spread) over the de-risked-cashflows-weighted-average of Fundamental Spreads over the life of the bond.Return-on-SCRExpected return divided by the dominant risk type SCR value.

Equity BSCREquity Bermuda Solvency Capital Requirement (BSCR) - an aggregated value from the next four entries.Equity Type 1Equity Type 1 BSCR - mainly DM Equties (scope of DM defined by Bermuda Monetary Authority).Equity Type 2Equity Type 2 BSCR - mainly EM Equities.Equity Type 3Equity Type 3 BSCR - infrastructure equity.Equity Type 4Equity Type 4 BSCR - real estate.Interest Rate BSCRInterest rate BSCR from all fixed income assets. Only one of rate-up and rate-down shocks is used.Fixed Income Risk BSCRFixed Income Risk BSCR - category- and rating-based.Currency Risk BSCRCurrency BSCR.Concentration Risk BSCRConcentration risk BSCR. Normally only calculated at total B/S level.Total Market Risk BSCRTotal market risk BSCR - an aggregate of equity, fixed income, interest rate, concentration and currency risks.Diversification BenefitDiversification Benefit - the difference between the arithmetic sum of the individual risk capital and the total market risk BSCR.Return-on-BSCRExpected return divided by the dominant risk type BSCR value.

Growth SSTGrowth asset price risk under the Swiss Solvency Test (SST) - an aggregated value from the next four entries. Note that aggregation is risk-factor-based rather than via a correlation matrix.EquityEquity price risk under the SST.Real EstateProperty price risk under the SST.Private EquityPrivate Equity price risk under the SST.Hedge FundHedge Fund price risk under the SST.Spread SSTCredit spread capital under the SST. Note that this is based on one or several credit risk factors.Interest Rate SSTInteret rate risk under the SST. Note that this is based on one or several interest rate risk factors.Currency Risk SSTCurrency capital under the SST.Pre-SceneMarket risk SST aggregated before the addition of any scenario-based risk capital.Scenario-SSTScenario-based risk capital add-ons under the regulatory-defined SST market risk scenarios.Market Risk SSTMarket risk SST aggregated including scenario-based risk capital.Diversification BenefitDiversification Benefit - the difference between the arithmetic sum of market and credit risk capital and the total market risk SST.Credit Default Risk SSTCredit default risk capital under the SST, calculated using BASEL III methods.Return-on-SSTExpected Return divided by the domnant component of SST risk capital.

Domestic Int Rate RiskDomestic market (China) interest rate risk. Note this is not calculated, but a user-given input in the SCR Calculator. The SCR Calculator currently only implements foreign asset risk types.Domes Growth Asset RiskDomestic market (China) growth asset price risk. Note this is not calculated, but a user-given input in the SCR Calculator. The SCR Calculator currently only implements foreign asset risk types.Domes Real Estate RiskDomestic market (China) real estate price risk. Note this is not calculated, but a user-given input in the SCR Calculator. The SCR Calculator currently only implements foreign asset risk types.Emerging Market Fixed IncomeEmerging market (ex-China) fixed income asset price risk.Dev Market Fixed IncomeDeveloped market fixed income asset price risk.EM Growth Asset RiskEmerging market (ex-China) growth asset price risk.DM Growth Asset RiskDeveloped market growth asset price risk.Currency RiskForeign currency risk from CNY perspective.Total Market RiskTotal market risk, an aggregated value from all the market risk components.Diversification BenefitDiversification Benefit - the difference between the arithmetic sum of the market risk components and the total market risk risk capital.Return-on-Reg CapitalExpected Return divided by the domnant component of market risk capital.

Equity Risk CapitalEquity price level risk and volatility risk for options.Property Risk CapitalProperty price level risk.Spread Risk CapitalSpread widening risk.Real Interest Rate UpReal interest rate up risk.Real Interest Rate DownReal interest rate down risk.Expected Inflation UpExpected inflation up risk, relevant for nominal bonds.Expectred Inflation DownExpected inflation down risk, relevant for nominal bonds.Currency Up RiskCurrency up risk (against AUD).Currency Down RiskCurrency down risk (against AUD).Total Market Risk CapitalTotal market risk, an aggregated value from the individual market risk components.Diversification BenefitDiversification Benefit - the difference between the arithmetic sum of the market risk components and the total market risk risk capital.Return-on-Reg CapitalExpected Return divided by the domnant component of market risk capital.

Equity Risk ChargeEquity risk charge.Property Risk ChargeProperty risk charge.Bond Market Risk ChargeBond market risk charge.Bond Credit Risk ChargeBond credit default risk charge.Total S&P CapitalTotal market and credit risk capital charge.Diversification BenefitDiversification Benefit - the difference between the arithmetic sum of the market risk components and the total market risk risk capital.Return-on-Reg CapitalExpected Return divided by the domnant component of market/credit risk capital.

EquityEquity risk capital - an aggregated value of equity level and volatility risks.Equity DMDM listed Equties risk capital.Equity EMEM listed Equities risk capital.Equity HybridPreferred Equities / Hybrid Bonds risk capital.Equity OtherRisk capital on other Equities - Hedge Funds, Private Equities, etc.Eq LevelEq Level risk - an aggregated value from the previous four components.Eq VolEquity volatility up risk.Int Rate Risk CapitalInterest rate risk (through stochastic simulation).Spread Up RiskNon-Default Credit Spread up risk.Spread Down RiskNon-Default Credit Spread down risk.PropProperty price risk.Currency RiskCurrency risk.Concentration RiskConcentration risk.Total Market Risk CapitalTotal market risk capital charge.Diversification BenefitDiversification Benefit - the difference between the arithmetic sum of the market risk components and the total market risk risk capital.Credit Default RiskCredit default risk capital.Return-on-Reg CapitalExpected Return divided by the domnant component of market risk capital.

Equity RiskEquity risk capital charge.Interest Rate RiskInterest rate risk calibrated through risk free curve shocks up/down.Spread RiskCredit Spread up risk calibrated through spread widening stress.Property RiskProperty price risk.Currency RiskCurrency risk for all non-SGD currency exposures.Total Market RiskTotal market risk capital charge.Diversification BenefitDiversification Benefit - the difference between the arithmetic sum of the market risk components and the total market risk risk capital.Return-on-Reg CapitalExpected Return divided by the domnant component of market risk capital.

Equity RiskEquity risk capital charge.Property RiskProperty risk capital charge.Fixed Income RiskFixed income risk charge, applicable to all fixed income assets on a notch-basis.Currency RiskCurrency risk capital charge, based on currency of the insurance contract and of the hypothecating assets.Concentration RiskConcentration risk applicable to all assets except for cash and government bonds. Calculated using Herfindahl_Scaler.Total Market RiskTotal market risk capital charge.Diversification BenefitDiversification Benefit - the difference between the arithmetic sum of the market risk components and the total market risk risk capital.Return-on-Reg CapitalExpected return divided by the dominant component of market risk capital.

Equity Risk PCREquity risk capital charge.Interest Rate Risk PCRInterest rate risk calibrated through risk free curve shocks up/down.Spread Widening Risk PCRCredit Spread up risk calibrated through spread widening stress.Property Risk PCRProperty price risk.Currency Risk PCRCurrency risk for all non-HKD currency exposures.Total market risk capital chargeTotal market risk capital charge.Diversification Benefit PCRDiversification Benefit - the difference between the arithmetic sum of the market risk components and the total market risk risk capital.Return on Regulatory CapitalExpected return divided by the dominant component of market risk capital.