SCR Calculator User Manual

Version 1.17 Last modified 2025-4-6

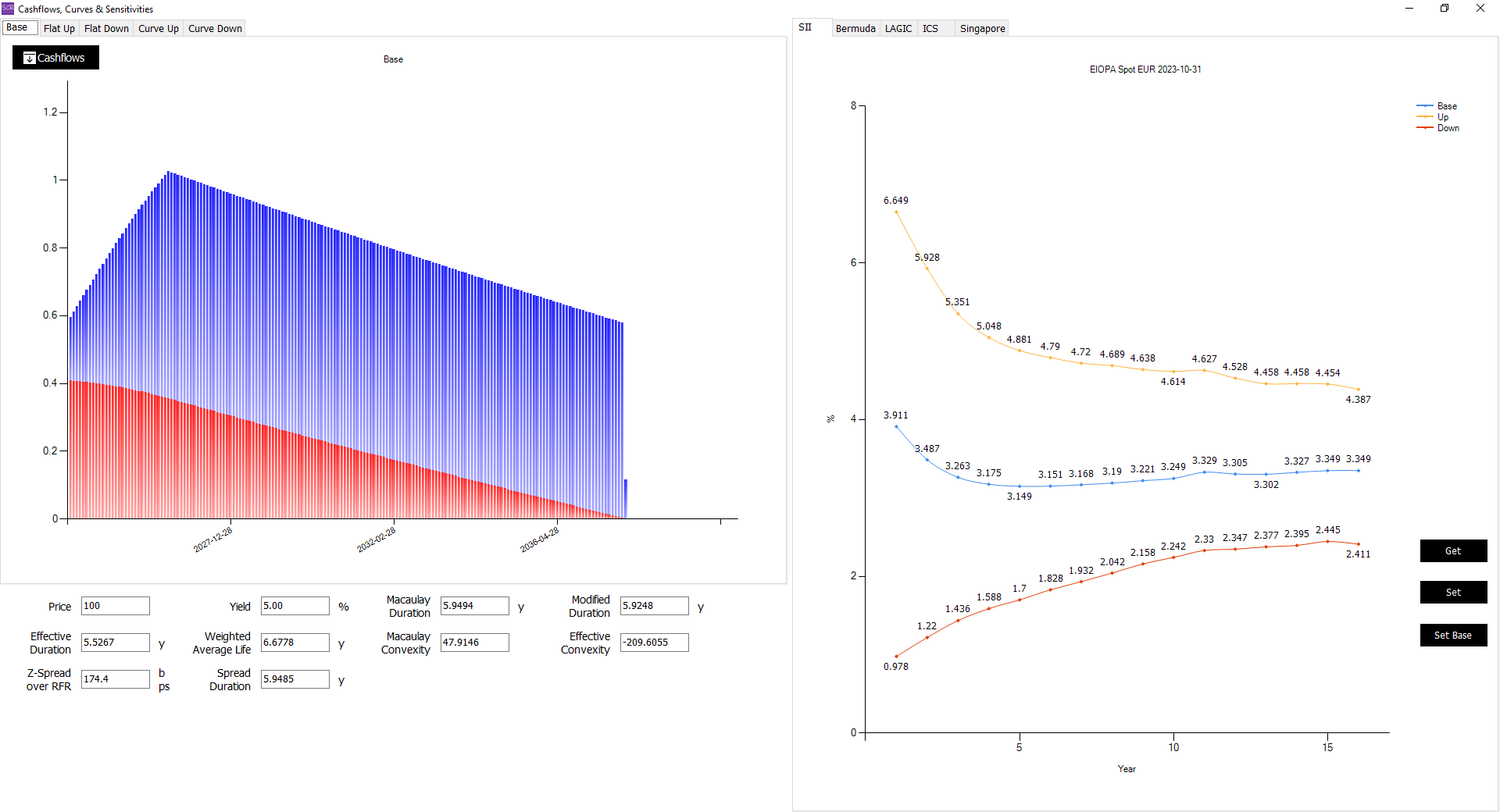

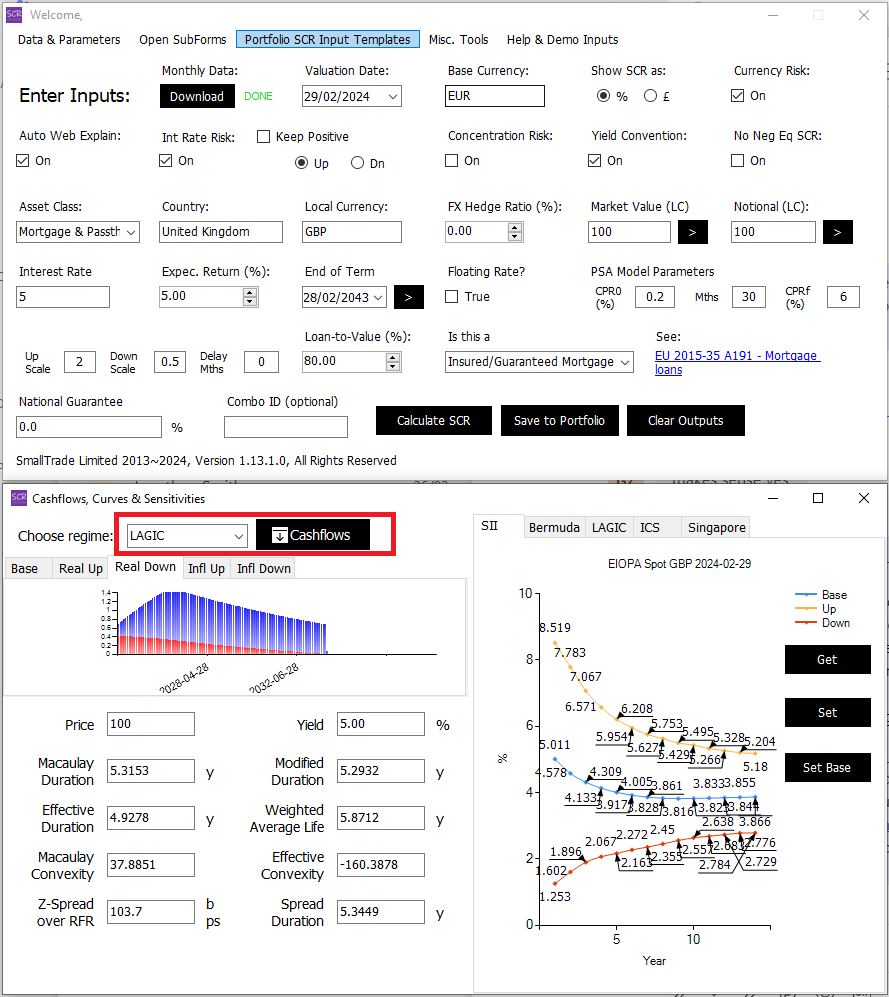

Cashflows, Curves & Sensitivities

The Cashflows, Curves & Sensitivities panel appears below the main form and serves several purposes:

- For fixed income assets, it models cashflows and calculates bond metrics such as duration, convexity, and other sensitivities.

- For equity options, it uses the Black-Scholes formula to calibrate implied volatility.

- For CDS, it goal-seeks the implied annual default rate.

A dropdown menu allows you to select the regime, and all cashflows and curves can be downloaded for further analysis:

For callable or puttable bonds, the downloaded spreadsheet includes additional tabs like "CallPutPV_Base," "CallPutPV_CurveUp," and "CallPutPV_CurveDown." These tabs contain present value parameters used to determine the most likely option exercised and the corresponding cashflows. For more details, refer to Appendix II.1: Modelled Cashflows with Optionality.

While this panel supports the SCR calculations described earlier, it also offers additional functionalities:

- Estimate yield and sensitivities for fixed income assets when only basic details like coupon and maturity are provided, often the case with private debt.

- Calculate variable cashflows of floating rate assets under different yield curve scenarios.

- Analyze rate sensitivity and cashflow patterns of complex assets like mortgages.

The panel is designed as an independent form, allowing you to enlarge it for a detailed view of cashflows and curves.