SCR Calculator User Manual

Version 1.17 Last modified 2025-4-6

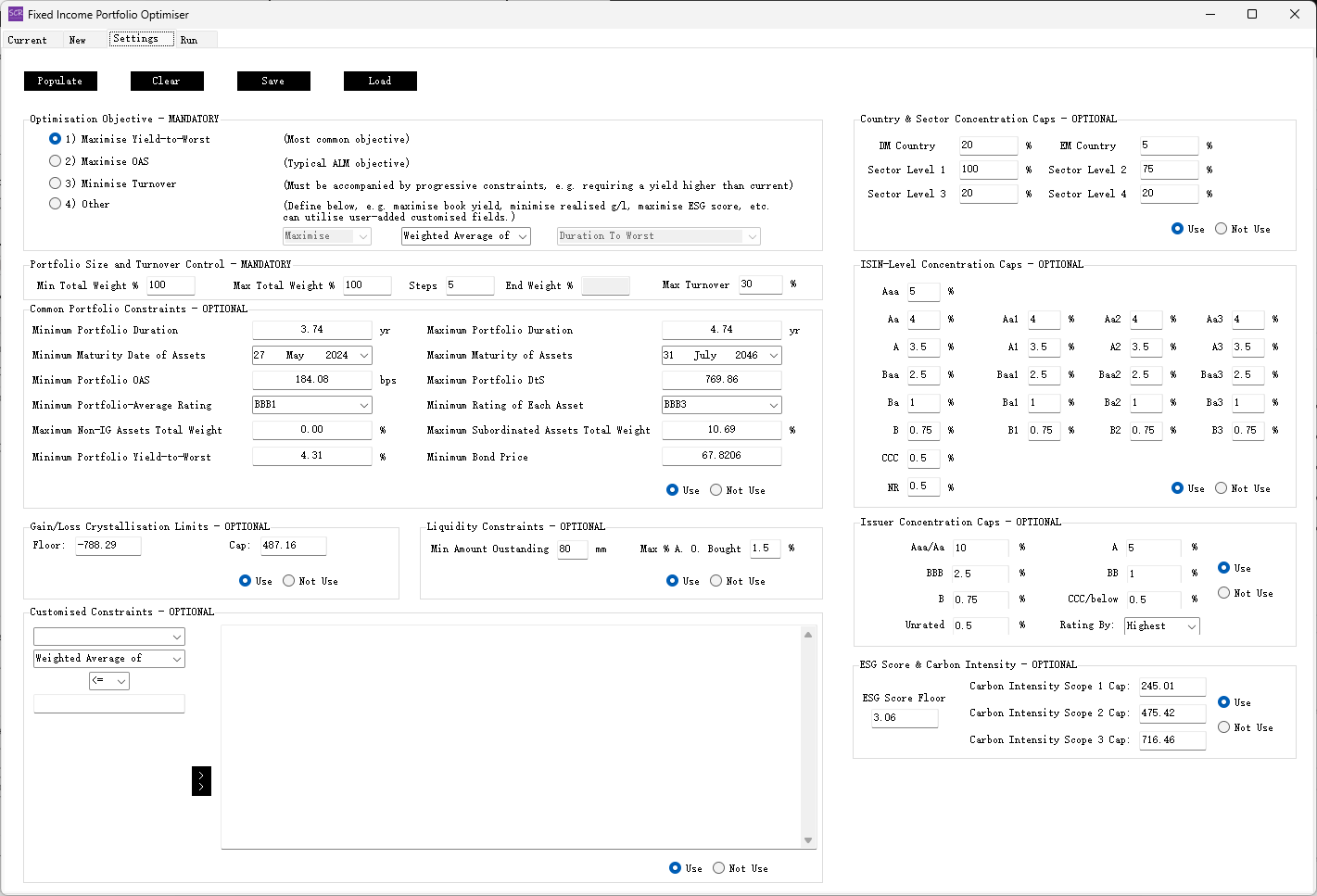

The 'Settings' Tab

The 'Settings' tab provides essential parameters and controls for optimisation. It is organised into several mandatory and optional sections, as shown in the screenshot below:

(Open this image in a new tab for an enlarged view)

The Four Buttons at the Top

Populate: Populates all input fields in this tab. Defaults are typically based on the current portfolio's values.Clear: Clears all input fields in this tab.Save: Saves the input values to a "Settings" spreadsheet.Load: Loads a "Settings" spreadsheet to populate the input fields.

Optimisation Objective - MANDATORY

The user must select one of the following four options:

Maximise Yield-to-Worst: The most common fixed-income portfolio optimisation objective.Maximise OAS: Focuses on Option-Adjusted Spread, useful when liabilities are discounted using risk-free swap or government bond curves.Minimise Turnover: Ideal when aiming for higher yield than the current portfolio while limiting turnover.Other: Allows custom objectives based on user-defined fields, such as:- Maximising

Book Yieldby selecting it as a weighted-average objective if included in the inputsheet. - Maximising

ESG Scoresif the "ESG Score" column is provided, using the weighted-average method. - Maximising cashflows for a specific year by creating a custom cashflow column and using the proportional-sum method.

- Minimising realised gain for tax purposes by maximising the

Unrealised Gain/Losscolumn with proportional-sum selected.

- Maximising

Portfolio Size and Turnover Control - MANDATORY

This section includes two key controls:

Min Total Weight %andMax Total Weight %:- Set both to 100% to maintain the portfolio size.

- Enter a consistent value (e.g., 120%) to grow or shrink the portfolio size to a fixed level.

- Set a range (e.g., 60%-120%) to allow the optimiser to search for an optimal portfolio size. The final weight will be displayed in

End Weight %after optimisation.

Max Turnover: Default is 30%. Defines the maximum percentage of the current portfolio that can be sold. New purchases are not counted as turnover.

Common Portfolio Constraints - OPTIONAL

This section includes commonly used constraints, such as:

Minimum Portfolio DurationandMaximum Portfolio Duration: Weighted-average duration range. Defaults to ±0.5 around the current portfolio's duration.Minimum Maturity DateandMaximum Maturity Date: Asset-level maturity constraints.Minimum Portfolio OAS: Weighted-average Option-Adjusted Spread lower bound.Maximum Portfolio DtS: Upper bound for weighted-average Duration-times-Spread.Minimum Portfolio-Average Rating: Weighted-average credit rating minimum (notch-level).Minimum Rating of Each Asset: Lowest rating allowed for individual assets.Maximum Non-IG Assets WeightandMaximum Subordinated Assets Weight: Constraints on portfolio composition.Minimum Portfolio Yield-to-Worst: Minimum Yield-to-Worst of the portfolio.Minimum Bond Price: Filters out near-default bonds with low prices and high yields.

Gain/Loss Crystallisation Limits - OPTIONAL

Applicable if the Unrealised Gain/Loss column is included in the inputsheet.

This section allows the user to manage P&L crystallisation during rebalancing with Floor and Cap values.

Liquidity Constraints - OPTIONAL

Requires the Amount Outstanding column in the inputsheet. Constraints include:

Min Amount Outstanding: Minimum liquidity threshold (in millions).Max % A.O. Bought: Maximum allowable purchase of any issuance’s outstanding amount.

Country & Sector Concentration Caps - OPTIONAL

DM CountryandEM Country: Allocation caps for developed and emerging market countries.Sector Level 1,2,3,4: Allocation caps for industry sectors.

ISIN-level Concentration Caps - OPTIONAL

Set concentration limits based on asset ratings or notches, if needed.

Issuer Concentration Caps - OPTIONAL

Define caps at the ticker level. The user can choose to rate issuers by the highest rating of their issues or their weighted average. Default is 'Highest.'

ESG Score & Carbon Intensity - OPTIONAL

Applicable only if relevant columns are included in the inputsheet. Defaults are based on the current portfolio's values.

Customised Constraints - OPTIONAL

Allows constraints on arbitrary columns.

- For numeric columns, constraints can be based on weighted averages or proportional sums. The latter is suitable for cashflow constraints.

- For non-numeric columns, users can select specific entries to define constraints on their combined weights.