SCR Calculator User Manual

Version 1.17 Last modified 2025-4-6

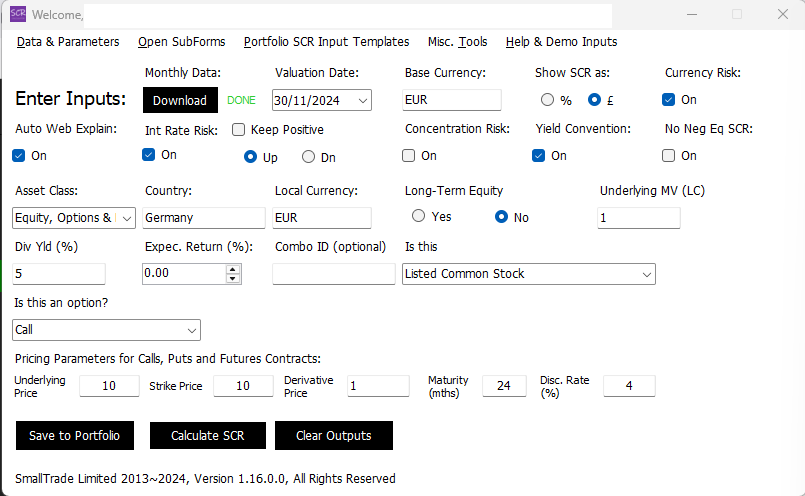

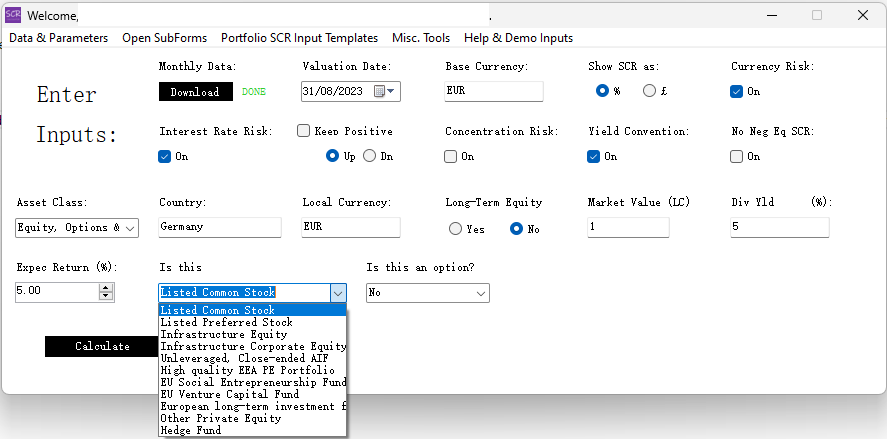

Equity, Equity Options & Hedge Funds

Equity

Equities attract different levels of SCR based on their specific type. Hedge funds are generally classified as equities, with leveraged hedge funds incurring higher capital charges than regular equities.

Dividend yield data can be useful in several contexts, such as estimating capital charges under Australian LAGIC, representing cash yield within a portfolio, or supporting Black-Scholes calculations for equity option SCRs.

Equity Futures, and Puts/Calls

For derivatives such as futures or puts/calls, you must specify the type of contract ("call," "put," or "future") and enter the notional value. The sign of the notional determines the position:

- A positive notional indicates a long position.

- A negative notional indicates a short position.

For equity options, additional inputs are required:

- Underlying Equity Price and Strike Price to determine the option's "moneyness."

- Option Price, Maturity, and Discount Rate, along with the previously entered Dividend Yield, to calibrate implied volatility.

- Only European options are currently supported.