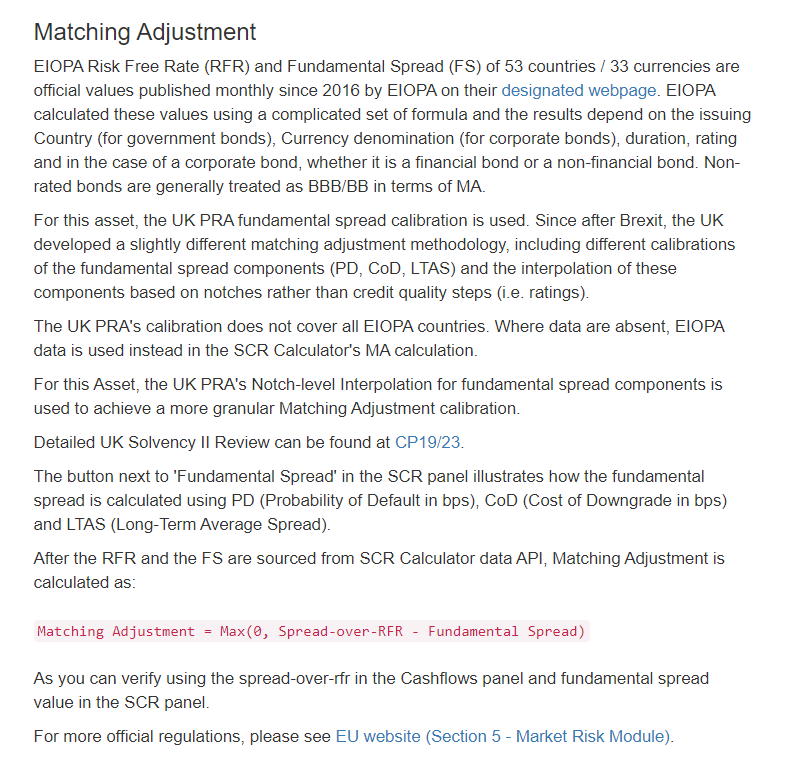

SCR Calculator User Manual

Version 1.17 Last modified 2025-4-6

Notch-level Interpolation

Using the UK PRA's MA MethodologyWhen 'PRA' is selected, the SCR Calculator will:

- Use the UK PRA's published risk-free rates, fundamental spread components (probability of default, cost of downgrade, long-term average spreads), and symmetric adjustments wherever available. (These datasets are stored in the SCR Calculator's database and accessed via its API.) Note that the UK PRA provides data for fewer countries compared to EIOPA and typically releases it later in the month (around the 8th, versus EIOPA's release around the 5th). If UK PRA data is unavailable, EIOPA data is used instead.

- Apply the UK PRA's notch-level interpolation methodology for fundamental spread components where applicable.

How the Interpolation Works

- Interpolation is applied only for corporate or covered bonds (not government bonds) with ratings that are not central notches (e.g., A1 or A3, but not A2) and are not rated AAA or CCC-and-below.

-

Fundamental spread components subject to interpolation include:

Probability of Default in bps (PD)Cost of Downgrade in bps (CoD)Long-Term Average Spread in bps (LTAS)

-

The fundamental spread (FS) is calculated as:

- For corporate bonds:

FS = max(PD + CoD, 0.35 * LTAS)(interpolated components used as needed). - For government bonds:

FS = max(PD + CoD, 0.3 * LTAS)(components remain at the rating level, no interpolation).

- For corporate bonds:

-

For an "upper" notch corporate or covered bond, the FS components are calculated as a weighted average:

PD (AA1) = 1/3 * PD (AA) + 2/3 * PD (A)CoD (AA1) = 1/3 * CoD (AA) + 2/3 * CoD (A)LTAS (AA1) = 1/3 * LTAS (AA) + 2/3 * LTAS (A)

- This method, known as the "full component interpolation method," is used in the SCR Calculator. The simplified method (PD + overall) described by the UK PRA is not implemented, as it is less precise.

Explanatory Notes

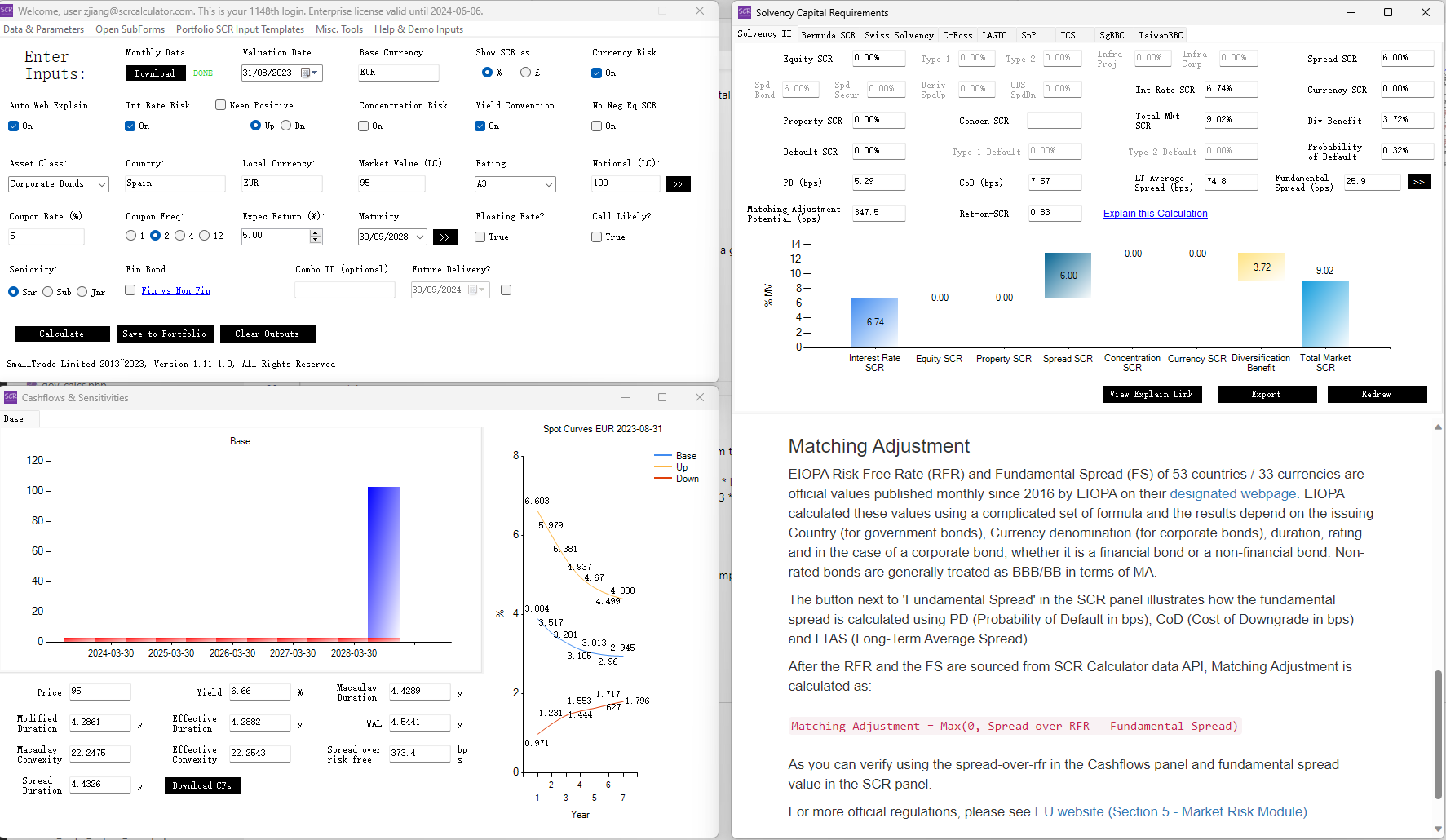

If notch-level interpolation is applied, the explanatory notes in the single asset panel will notify the user. Below are examples for a Spanish A1-rated corporate bond:

Inputs and explanatory notes under the EIOPA methodology:

Explanatory notes under the PRA interpolation methodology: