SCR Calculator User Manual

Version 1.17 Last modified 2025-4-6

Step 5: Add Verbal Constraint(s)

Verbal constraints allow you to define relationships between asset class weights, which can be essential for implementing specific allocation policies.

Let’s make the following changes in the constraint settings panel:

-

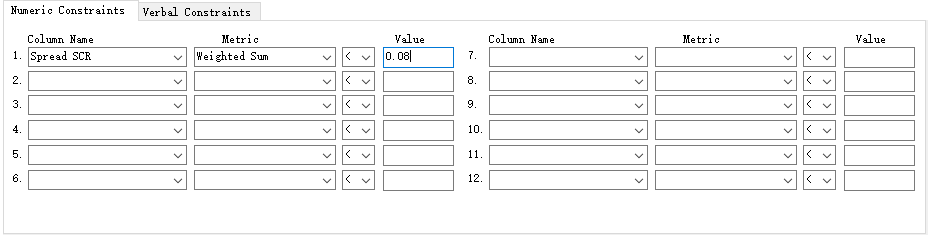

Relax the

SCR Spreadconstraint to 0.08 to create additional capital headroom:

-

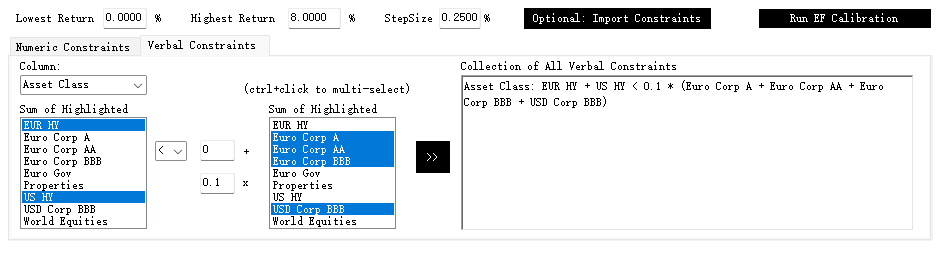

Constrain the combined weight of

[EUR + US] HYto be ≤ 1/10 of the combined weight of[AA + A + BBB]corporate bonds. To set this up:- Switch to the

"Verbal Constraint"tab. - Use

Ctrl + Clickto multi-select items. - Enter coefficients, as shown below.

- Click the double right arrow button to add the constraint to the right-hand-side box.

- Switch to the

-

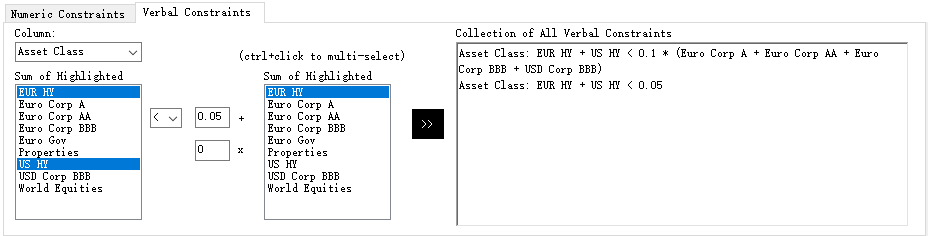

Constrain the combined weight of

[EUR + US] HYto be ≤ 0.05 of the total portfolio. Enter the settings as shown below and click the double right arrow again to add another verbal constraint:

The two small boxes in the middle of the panel allow you to apply constant addition or multiplication parameters.

You can add multiple verbal constraints, each on a new line. While manual editing of constraints in the right-hand-side box is possible, it is error-prone and not recommended.

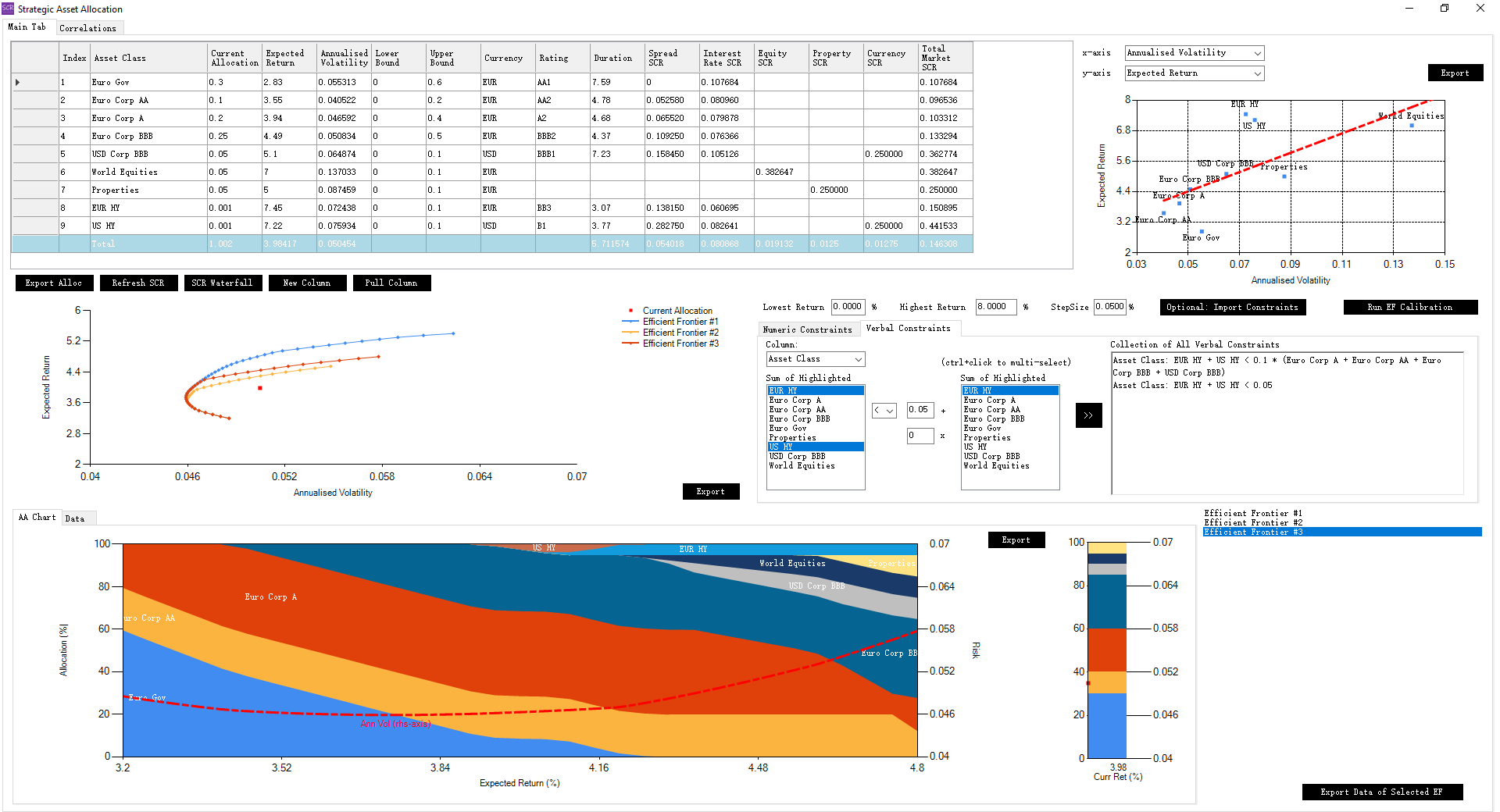

Now click the "Run EF" button again. This generates EF #3 (red), which falls between EF #1 and EF #2:

EF #3 reflects a set of constraints closely aligned with actual allocation policies, considering both risk appetite and capital budgets. Examining its mid-to-high target return allocations in the Stacked Area chart reveals that EUR HY (light blue) tends to dominate over US HY (brown).

Key takeaway: Based on historical asset correlations, volatilities, forward-looking expected returns, and defined risk/return/capital constraints, EUR HY is more beneficial for the balance sheet than US HY.