SCR Calculator User Manual

Version 1.17 Last modified 2025-4-6

The SCR Tabs

The remaining tabs—"SII," "BSCR," "SST," "C-ROSS," "LAGIC," "SnP," "ICS," etc.—are collectively referred to as "SCR Tabs" because they display Solvency Capital Requirement (SCR) figures under different regulatory regimes.

Note that Japan-ESR and K-ICS, as variations of the ICS framework, are not displayed directly. To calculate and view them, go to the Main Form, navigate to "Data & Parameters" → "Specific Parameters" → "ICS Regime Choice," and select either "K-ICS" or "Japan-ESR." This action ensures that all ICS calculations align with the selected framework.

Portfolio-Level Data

SCR figures in these tabs are derived from line-level calculations performed on all portfolio assets. The results are then aggregated to the portfolio level using the respective correlation matrices. Additional details on these regime-specific aggregations are included in the Appendices.

Line-Level Data

You can enable line-level data by ticking the checkbox next to a textbox. These SCR figures, expressed as a proportion of asset values, are particularly useful for detailed analysis. Once added to the main table, line-level data can be exported using the "Export Table" button on the right-hand side.

Specific Risk Reports

Some risk capital calculations are highly complex, and dedicated reports are provided for clarity. For example, if you opt to calculate concentration risk in the Welcome Form (default is off), a "+" button will appear next to the "Concentration Risk" textbox in the "Solvency II" tab. Clicking this button generates a CSV report detailing names, weights of in-scope and out-of-scope positions, and their contributions to the Concentration Risk SCR.

Similarly, the "ICS" tab includes buttons for generating reports on interest rate and concentration risk calculations.

Detailed Explanations

Below, you will find explanations for the textboxes in each of the SCR tabs:

"SII" TabEquity SCR: Solvency Capital Requirement (SCR) for equity investments, calculated as an aggregate of the following four entries.Equity Type 1: Includes primarily developed market traded equities and certain private equity funds with special classifications.Equity Type 2: Covers emerging market equities, hedge funds, and most private equity investments.Infra Proj: SCR for infrastructure project equity, which benefits from capital relief under Solvency II.Infra Corp: SCR for infrastructure corporate equity, which also enjoys capital relief but less so than project equity.Spread SCR: Spread risk SCR, an aggregate of the following four entries.Bond: Spread SCR for credit bonds.Securi: Spread SCR for securitized positions.CDS SpdUp: Spread SCR for credit default swaps under the spread-up shock (only one of spread-up or spread-down shocks is used).CDS SpdDn: Spread SCR for credit default swaps under the spread-down shock (only one of spread-up or spread-down shocks is used).Int Up SCR: Interest rate SCR for all fixed income assets under the rate-up scenario (only one of rate-up or rate-down scenarios is used).Int Dn SCR: Interest rate SCR for all fixed income assets under the rate-down scenario (only one of rate-up or rate-down scenarios is used).Currency SCR: SCR for currency risk.Property SCR: SCR for property investments.Concen SCR: Concentration risk SCR, typically calculated at the total balance sheet level.Total Mkt: Total market risk SCR, aggregating equity, property, spread, interest rate, concentration, and currency risks.Divers Ben: Diversification benefit, representing the reduction between the arithmetic sum of individual risk capitals and the total market risk SCR.Default SCR: Counterparty default SCR, an aggregate of the next two entries.Type 1 Default: Counterparty default SCR for Type 1 exposures.Type 2 Default: Counterparty default SCR for Type 2 exposures.RoSCR: Return-on-SCR.-

MA Potent: Matching Adjustment (MA) potential of eligible assets, expressed as a percentage. Selecting the checkbox beside this field adds additional MA-related data fields to the main table:MA: Matching Adjustment, calculated as the Z-Spread over the risk-free rate minus the fundamental spread.DurXMA: Duration multiplied by the Matching Adjustment, useful for optimization purposes.PDprob: Probability of Default (in %) for each year over the bond's life, provided in a comma-delimited format.PDpct: Probability of Default (in bps) for each year over the bond's life, used for fundamental spread calculations.CoD: Cost of Downgrade (in bps) for each year over the bond's life, used for fundamental spread calculations.LTAS: Long-Term Average Spread (in bps) for each year over the bond's life, used for fundamental spread calculations.FS: Fundamental Spread value for each year over the bond's life, as provided by regulatory bodies (EIOPA or PRA).

-

MA Assets: Weight of Matching Adjustment assets within the portfolio. Selecting the checkbox beside this field adds PRA-specific MA-related data fields to the main table:PDprob_BetterandPDprob_Worse: Interpolated probabilities of default (in %).PDpct_BetterandPDpct_Worse: Interpolated probabilities of default (in bps), for UK-PRA fundamental spread calculations.CoD_BetterandCoD_Worse: Interpolated costs of downgrade (in bps), for UK-PRA fundamental spread calculations.LTAS_BetterandLTAS_Worse: Interpolated long-term average spreads (in bps), for UK-PRA fundamental spread calculations.FS_BetterandFS_Worse: Interpolated fundamental spread values, verifying that interpolated values lie within this range.

Equity BSCR: Bermuda Solvency Capital Requirement (BSCR) for equities, aggregated from the following four categories.Equity Type I: BSCR for developed market equities, as defined by the Bermuda Monetary Authority.Equity Type II: BSCR for emerging market equities.Equity Type III: BSCR for infrastructure equity investments.Equity Type IV: BSCR for real estate investments.FI BSCR: Fixed income risk BSCR, based on categories and ratings.Int Up BSCR: BSCR for interest rate risk under the rate-up scenario (only one of rate-up or rate-down scenarios is used).Int Dn BSCR: BSCR for interest rate risk under the rate-down scenario (only one of rate-up or rate-down scenarios is used).Currency BSCR: BSCR for currency risk.Concen BSCR: BSCR for concentration risk, typically calculated at the total balance sheet level.Total Mkt: Total market risk BSCR, aggregating equity, fixed income, interest rate, concentration, and currency risks.Divers Ben: Diversification benefit, representing the difference between the sum of individual risk capitals and the total market risk BSCR.RoBSCR: Return-on-BSCR.

Growth SST: Growth asset price risk under the Swiss Solvency Test (SST), aggregated from the following four categories. Aggregation is based on risk factors, not correlation matrices.Equity: Equity price risk under the SST.Property: Property price risk under the SST.Hedge Fund: Hedge fund price risk under the SST.Private Equity: Private equity price risk under the SST.Int Rate SST: Interest rate risk under the SST, based on one or more risk factors.Currency SST: Currency risk capital under the SST.Spread SST: Credit spread risk capital under the SST, based on one or more credit risk factors.Pre-Scene: Market risk SST aggregated before including scenario-based risk capital.Scene-SST: Scenario-based risk capital under regulatory-defined SST market risk scenarios.Market SST: Market risk SST, aggregated with scenario-based risk capital.Credit SST: Credit default risk capital under the SST, calculated using Basel III methods.Total SST: Total aggregation of market and credit risk capital under the SST.Divers Ben: Diversification benefit, calculated as the difference between the sum of individual market and credit risks and the total market risk SST.RoSST: Return-on-SST capital.

EM Growth: Price risk for emerging market (excluding China) growth assets.DM Growth: Price risk for developed market growth assets.DM FI: Price risk for developed market fixed income assets.EM FI: Price risk for emerging market (excluding China) fixed income assets.FX: Foreign exchange risk, from the perspective of the Chinese yuan (CNY).Domes IntRate: Domestic (China) interest rate risk. Note: This is a user-provided input, not calculated by the SCR Calculator.Domes Growth: Domestic (China) growth asset price risk. Note: This is a user-provided input, not calculated by the SCR Calculator.Domes Real Estate: Domestic (China) real estate price risk. Note: This is a user-provided input, not calculated by the SCR Calculator.Total Market: Total market risk, aggregated from the above six categories.Divers Ben: Diversification benefit, calculated as the difference between the sum of the six market risks and the total market risk capital.

Equity: Risk associated with equity price fluctuations.Property: Risk related to property price changes.Spread: Risk due to spread widening in credit markets.Real Int Up: Risk from an increase in real interest rates.Real Int Dn: Risk from a decrease in real interest rates.Exp Int Up: Risk from a rise in expected inflation.Exp Int Dn: Risk from a drop in expected inflation.Currency Up: Risk from an appreciation of foreign currencies against the AUD.Currency Down: Risk from a depreciation of foreign currencies against the AUD.Total Market: Aggregated total market risk, combining all individual components.Divers Ben: Diversification Benefit - the difference between the sum of individual risks and the total market risk capital.Ret-on-LAGIC: Return-on-capital requirement under the LAGIC framework.

Equity: Risk charge for equity investments.Property: Risk charge for property investments.Bond Credit: Risk charge for bond credit default.Bond Market: Risk charge for bond market fluctuations.Total Capital: Total risk capital charge, aggregating market and credit risks.Divers Ben: Diversification Benefit - the difference between the sum of individual risks and the total risk capital charge.Ret-on-Capital: Return-on-capital requirement under the S&P framework.

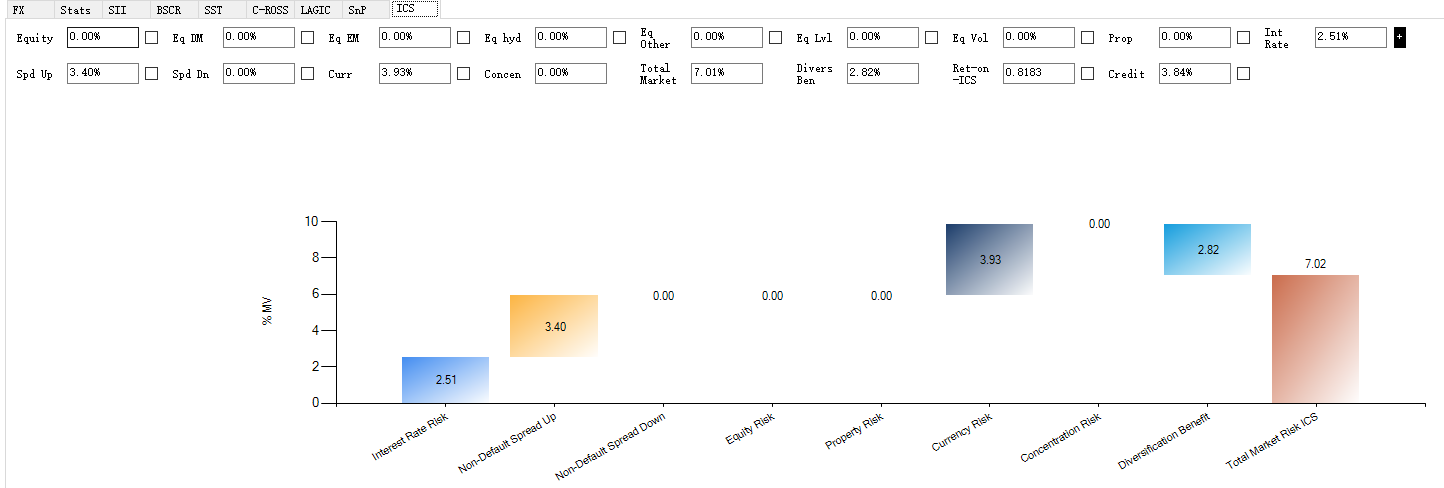

Equity: Total equity risk capital, including equity level and volatility risks.Equity DM: Risk capital for developed market listed equities.Equity EM: Risk capital for emerging market listed equities.Equity Hyd: Risk capital for preferred equities and hybrid bonds.Equity Other: Risk capital for other equity investments such as hedge funds and private equities.Eq Lvl: Aggregated equity level risk from the previous categories.Eq Vol: Risk due to equity volatility increases.Prop: Risk related to property price fluctuations.Int Rate: Risk associated with interest rate changes, assessed through stochastic simulation.Spd Up: Non-default credit spread widening risk.Spd Dn: Non-default credit spread tightening risk.Curr: Currency risk associated with foreign exchange movements.Concen: Concentration risk arising from portfolio imbalances.Total Capital: Total risk capital charge, combining market and credit risks.Divers Ben: Diversification Benefit - the difference between the sum of individual risks and the total risk capital charge.Ret-on-ICS: Return-on-capital requirement under the ICS framework.Credit: Risk capital for credit defaults.

Equity Risk: Capital charge for equity price risk.Interest Rate Risk: Risk from interest rate changes, calibrated using shocks to the risk-free curve (up/down).Spread Risk: Credit spread widening risk, calibrated using stress scenarios.Property Risk: Capital charge for property price risk.Currency Risk: Currency risk for exposures in all non-SGD currencies.Total Market Risk: Aggregated total market risk capital charge.Divers Ben: Diversification Benefit, calculated as the difference between the sum of individual risk components and the total market risk capital.RoRC: Return on Regulatory Capital.

Equity Risk: Capital charge for equity price risk.Property Risk: Capital charge for property price risk.Fixed Income Risk: Capital charge for fixed income assets, calculated on a notch basis.Currency Risk: Currency risk, based on the currency of insurance contracts and associated assets.Concentration Risk: Risk applicable to all assets except cash and government bonds.Total Market Risk: Aggregated total market risk capital charge.Divers Ben: Diversification Benefit, calculated as the difference between the sum of individual risk components and the total market risk capital.RoRC: Return on Regulatory Capital.

Equity Risk PCR: Capital charge for equity price risk.Interest Rate Risk PCR: Risk from interest rate changes, calibrated using shocks to the risk-free curve (up/down).Spread Widening Risk PCR: Credit spread widening risk, calibrated using stress scenarios.Property Risk PCR: Capital charge for property price risk.Currency Risk PCR: Currency risk for exposures in all non-HKD currencies.Total Market Risk PCR: Aggregated total market risk capital charge.Diversification Benefit PCR: Diversification Benefit, calculated as the difference between the sum of individual risk components and the total market risk capital.Return-on-PCR: Return on Regulatory Capital.

Equity Risk: Capital charge for equity price risk.Property Risk: Capital charge for property price risk.-

Interest Rate Risk DDD: Capital charge under the "DDD" scenario, involving decreased short-term interest rates, long-term interest rates, and ultimate interest rates (UIR). -

Interest Rate Risk UND: Capital charge under the "UND" scenario, involving increased short-term and long-term interest rates, and decreased UIR. -

Interest Rate Risk UUU: Capital charge under the "UUU" scenario, involving increased short-term, long-term, and ultimate interest rates. -

Interest Rate Risk DUU: Capital charge under the "DUU" scenario, involving decreased short-term and increased long-term and ultimate interest rates. Interest Rate Risk: The maximum capital charge among the four interest rate scenarios.Currency Risk: Risk for the larger of net long or net short foreign currency exposures.Total Market Risk: Aggregated total market risk capital charge as the sum of all components.Credit Risk: Default risk for fixed income assets, calibrated using a regulatory table for various asset categories.Return-on-LICAT: Return on Regulatory Capital under the LICAT framework.