SCR Calculator User Manual

Version 1.17 Last modified 2025-4-6

Overview

The Portfolio SCR Form enables calibration and reporting of a portfolio's SCR under multiple insurance regimes.

Using an Excel input template, it can process a TPT report and generate capital figures for various regulatory frameworks.

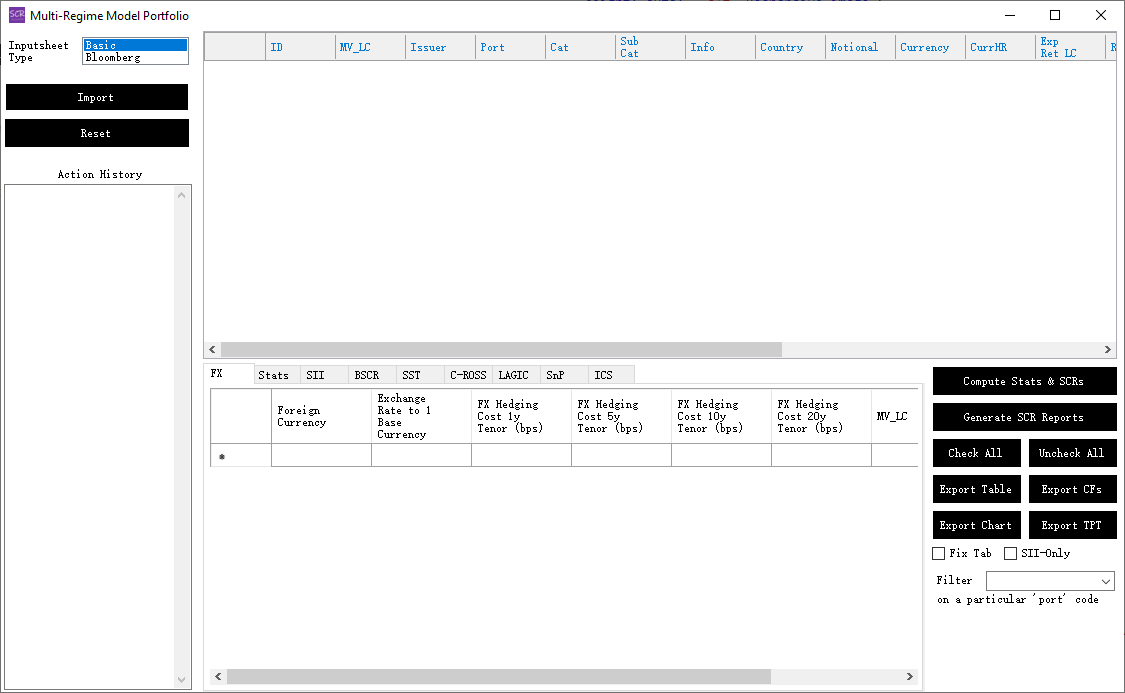

Opening the Form

From the main form menu, select "Open Subform" → "Portfolio SCR Calcs" to open a blank form:

This form is useful for:

- Accurately calculating SCR or producing solvency reports for an existing portfolio.

- Performing what-if analysis and sensitivity testing by adjusting asset weights.

- Integrating with the SAA form for optimization (covered in the next chapter).

The form is "single instance," meaning all data remains intact if you close and reopen it. To clear all data, use the "Reset" button.

You can set up a model portfolio in this form through several methods:

- Add individual assets from the Single Asset Form. Right-click to adjust an asset's market value, ensuring metrics like MV_PC (market value in porfolio currency) and Notional are updated accordingly.

- Import a Basic Inputsheet or a Bloomberg Inputsheet. Examples are available under Menu → "Model Portfolio templates."

The following sections describe the import methods in detail. Example input spreadsheets used in this chapter can be downloaded via Menu → Help → Download Demo Inputs.