SCR Calculator User Manual

Version 1.17 Last modified 2025-4-6

Run Optimisation

Once the 'Current' and 'New' tabs have been imported and the 'Settings' configured appropriately, navigate to the 'Run' tab and click the Run Optimisation button.

After a few seconds (depending on the complexity of constraints and your computer's processing speed, typically under one minute),

a message will indicate whether the optimisation was successful.

-

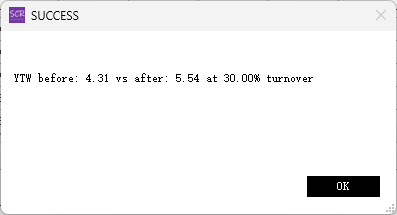

If optimisation succeeds, a before/after comparison of the objective metric will be displayed, for example:

- If optimisation fails, a technical error code will appear. This code may not provide actionable information, as failures are typically caused by overly restrictive constraints. The optimiser cannot pinpoint which specific constraint caused the issue, so the user must progressively loosen one or more constraints until optimisation succeeds. To avoid trial-and-error, it is recommended to set loose constraints initially and tighten them gradually.

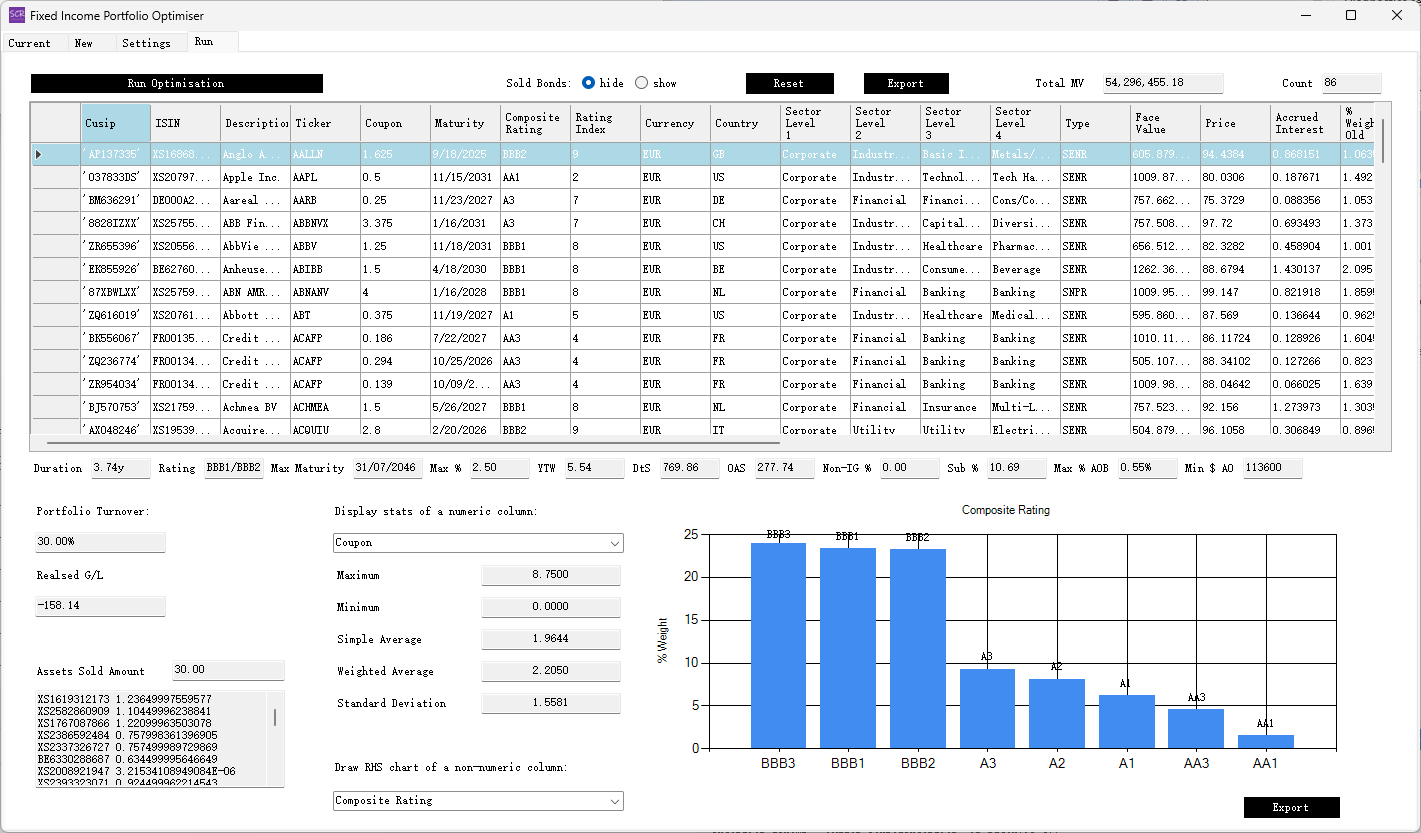

The layout of the 'Run' tab closely resembles the 'Current' and 'New' tabs, with the following differences:

- The datatable reflects the optimised portfolio. An additional column,

% Weight Old, is displayed alongside the% Weightcolumn. (Note: If a target portfolio weight different from 100% was set in the 'Settings,' the% Weightcolumn will sum to that target figure instead of 100%. This facilitates comparison.) - In the lower-left corner, controls specific to the optimisation are available:

Portfolio Turnover: Displays the actual turnover from the current portfolio to the optimised portfolio.Gain/Loss Crystallised: Shows the realised P&L from the turnover, which should fall within user-defined limits.Amount Sold: Represents the percentage of assets sold. A listbox below displays the sold items.

Iterations

Several iterations may be required to arrive at an ideal optimised portfolio. You can return to the 'Settings' tab, adjust the constraints, and re-run the optimisation in the 'Run' tab as needed.

The optimised portfolio serves as a robust starting point for constructing the final portfolio. Manual inspection and adjustments will still be necessary, but starting with an optimiser-generated portfolio often results in a more balanced outcome compared to building a portfolio entirely by hand.