SCR Calculator User Manual

Version 1.17 Last modified 2025-4-6

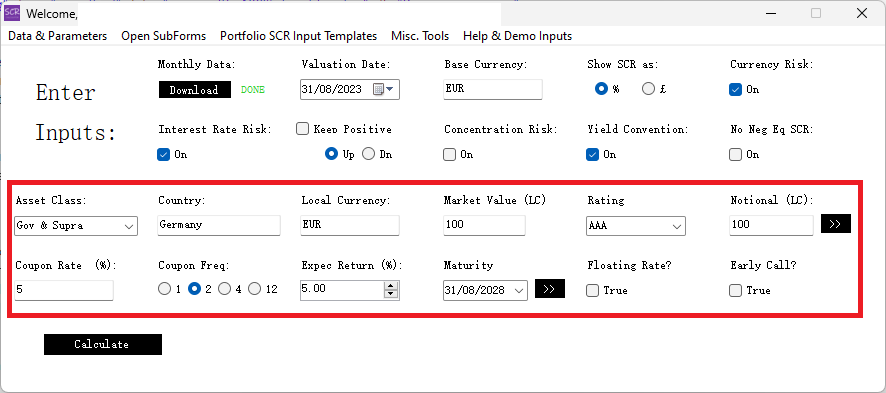

Government and Supranational Bonds

Here, we use government bonds to illustrate how the single asset SCR calculation works.

The calculator identifies required inputs based on the asset type and dynamically adjusts the layout as inputs are provided. It includes autocompletion for country, currency, and rating fields, along with basic input checks. If any input is incorrect or incomplete, the cursor will remain there until corrected.

For fixed income instruments, selecting a country automatically updates the rating input with the second-best rating from the Big Three agencies (from the calculator's internal database). If this default does not apply, such as for a corporate bond with a lower rating, you can manually adjust it. Once all inputs are complete, click 'Calculate.' If anything is missing, the calculator will prompt you.

The double arrow near the "Notional" field lets you calculate a bond's notional value based on its market value and price. Similarly, the double arrow near the "Maturity" field allows "goal-seeking" to find a hypothetical bond's maturity based on a specified duration—useful for proxying asset class indexes in SAA optimization.

Expected Return Explained

The "expected return" input is critical for return-on-SCR calculations and strategic asset allocation. While subjective, it often requires manual adjustments:

- For fixed income assets, the calculator auto-fills this value to match the coupon rate when entered. However, this is a suggestion, and you should update it as needed to avoid accidental changes.

- For floating rate bonds, manually set it to [margin + base rate]. (The "coupon rate" field will appear as "margin" for floating rate bonds.)

- For non-fixed-income assets, such as equities or properties, it is auto-filled with dividend yield or rental yield, which are not forward-looking. Replace this with a more realistic assumption.

Many leading asset managers provide Capital Market Assumptions to assist with setting expected returns.