SCR Calculator User Manual

Version 1.17 Last modified 2025-4-6

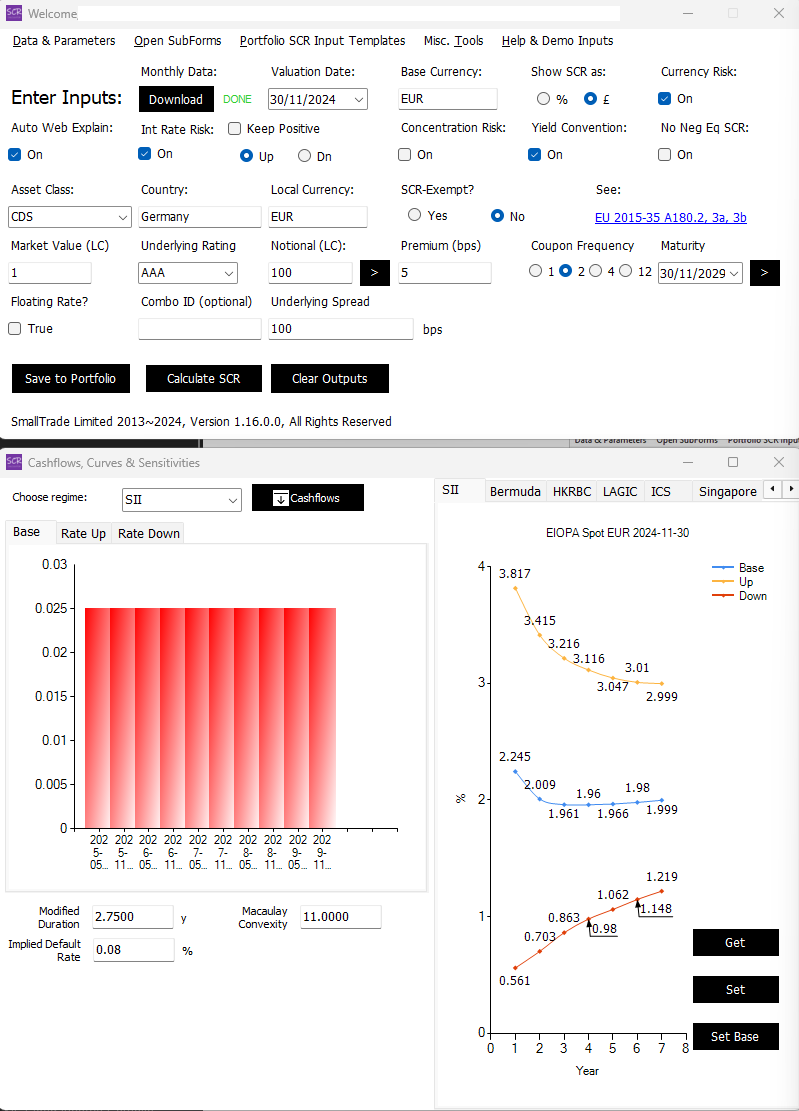

Credit Default Swap

Credit Default Swaps (CDS) are commonly used in insurance bond portfolios for risk management. You need to specify the notional and premium of the CDS contract, along with the rating and credit spread of the underlying asset. The sign of the notional determines whether the contract is a "Buy Protection" or "Sell Protection" arrangement:

- A positive notional indicates "Sell Protection / Receive Premium."

- A negative notional indicates "Buy Protection / Pay Premium."

CDS contracts are modeled using only the premium cashflows, while default payments are not included as actual cashflows. Instead, the impact of potential defaults is reflected in the market value of the CDS. The process works as follows:

- Premium payments or receipts are modeled based on the sign of the notional.

- The present value of these premium cashflows is calibrated to match the market value of the CDS, implicitly capturing the probabilistic default impact.

For a "Sell Protection / Receive Premium" CDS contract, the present value of premiums must exceed the contract's market value. If this condition is not satisfied, the calculator will flag the issue and request revised inputs.