SCR Calculator User Manual

Version 1.17 Last modified 2025-4-6

'Get' and 'Set' MA

Getting and Setting Fundamental Spread ComponentsNavigate to 'Menu' → 'Data & Parameters' → 'SII Fundamental Spread Parameters' to access the 'Get' and 'Set' functionalities for MA calculation.

'Get'

Clicking 'Get' downloads a spreadsheet containing all FS components for all currencies and economies:

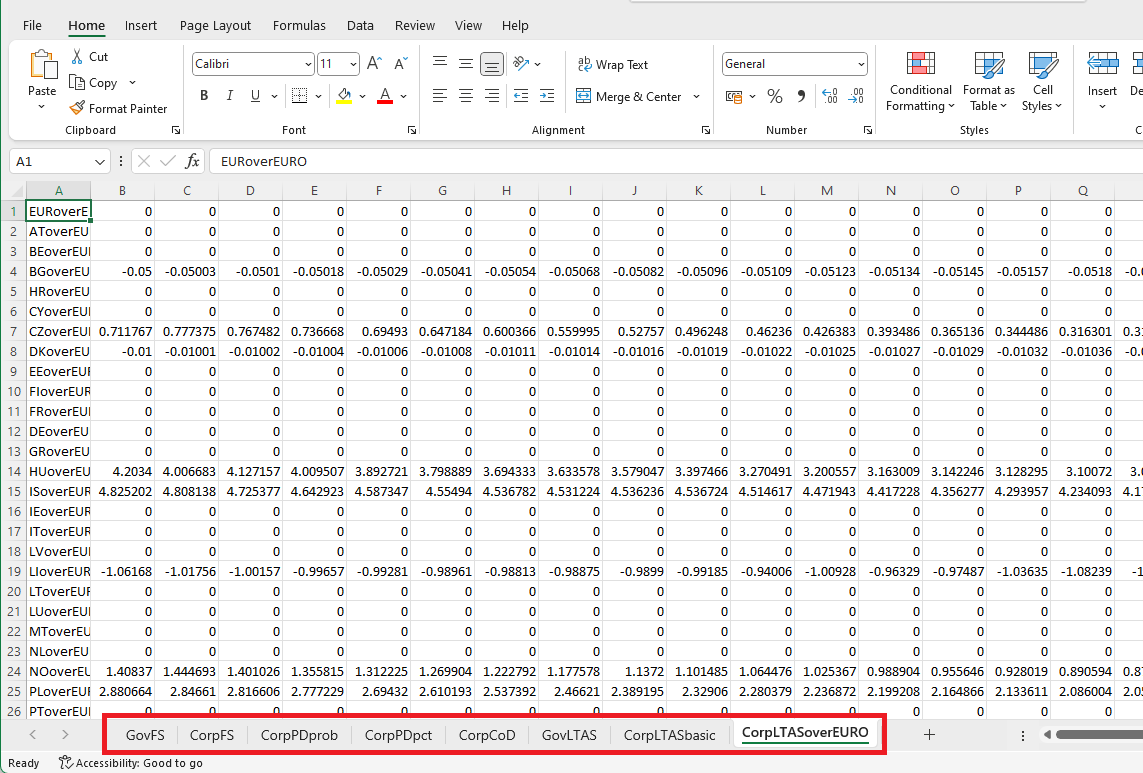

The downloaded spreadsheet includes the following tabs:

GovFS: Fundamental spreads for government bonds across 53 countries.CorpFS: Fundamental spreads for corporate bonds—14 rows per currency across 33 currencies, totaling 462 rows. Each currency has 7 financial and 7 non-financial bond FS values corresponding to CQS 0–7 (AAA to CCC-and-below).CorpPDprob: Probability of default for corporate bonds as percentages, used for cashflow haircuts in projections (462 rows).CorpPDpct: Probability of default for corporate bonds in bps, used for Fundamental Spread calculations (462 rows).CorpCoD: Cost of downgrade for corporate bonds, used for Fundamental Spread calculations (462 rows).GovLTAS: Long-term average spread for government bonds across 53 countries.CorpLTASbasic: Basic long-term average spread for corporate bonds published for EUR, USD, and GBP (42 rows total, 14 per currency).CorpLTASoverEURO: Long-term average spread over EUR for non-EUR currencies among the 53 selected countries. Calculated using the EIOPA formula:LTAS (currency i) = LTAS (EUR) + 0.5 * SpreadOverEURO.

'Set'

After modifying the spreadsheet, click 'Set' to upload it. Future calculations of the fundamental spread, and consequently the matching adjustment, will use these user-defined parameters.