SCR Calculator User Manual

Version 1.17 Last modified 2025-4-6

The New S&P Insurance Capital Post Nov-2023 - Implementation Technicals

Rating Agency Capital

Unlike other regulatory capital frameworks, the S&P Insurance Capital framework is a rating agency capital framework. It places emphasis more on the financial strength of the insurer than on policyholder protection - although the two are reflecting each other to a certain extent. Also, the quantitative aspects that are incorporated into the SCR Calculator is only the asset part of the total set of assessment rules in place.

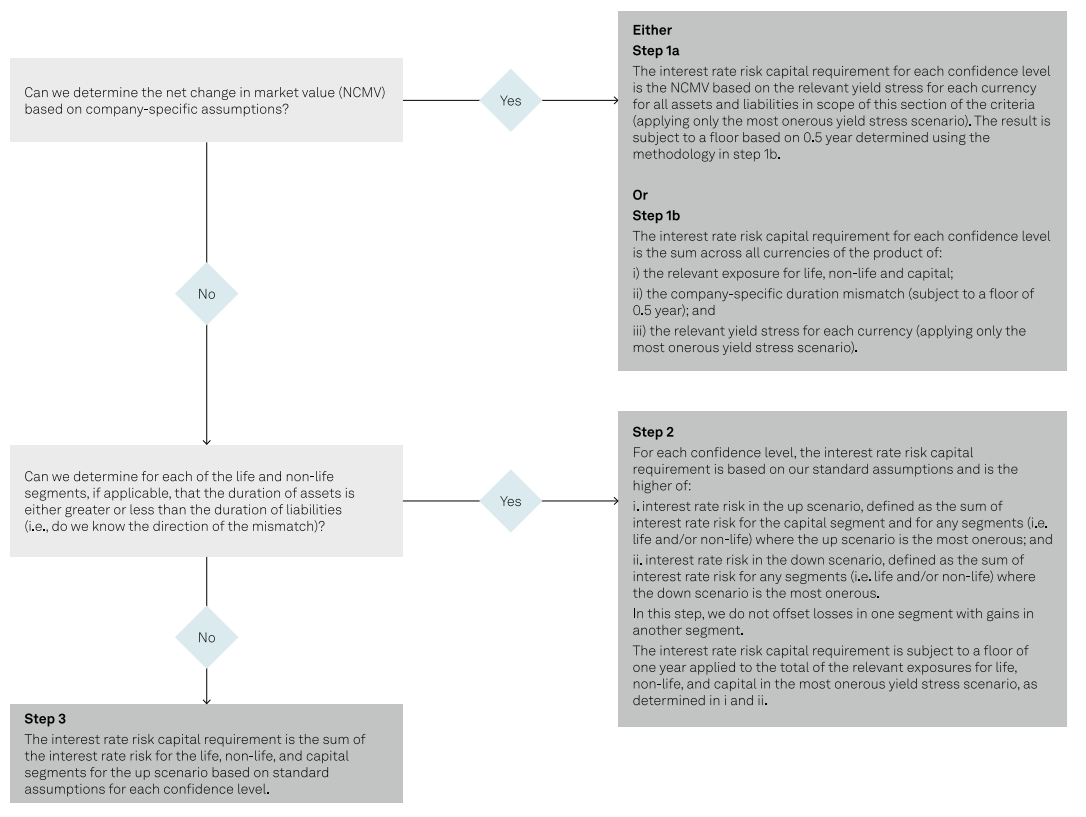

Interest Rate Risk Calculation

The interest rate market risk calculation allows for several types of simplifications. The Net Change in Market Value (NCMV) method is the most precise one. The other methods are listed in the following chart. All the methods require consideration of both assets and liabilities.

Single Asset Risk Capital

Single Asset Risk capital calculation is well-explained using the "Explain this Calculation" button.

Portfolio-level Risk Capital Aggregation

Portfolio-level Risk Capital Aggregation follows a 3-step process:

-

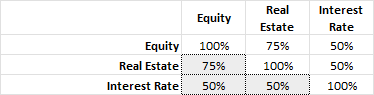

Level 1 Aggregation: The 3 market risks - 1) equity, 2) property, 3) interest rate - are first aggregated assuming the following correlation among them:

-

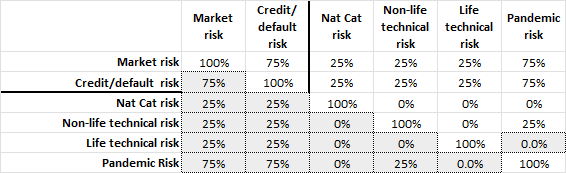

Level 2 Aggregation: Then market risk, credit risk and other non-asset risks are aggregated using the following larger correlation matrix:

-

Haircut to diversification: Depending on the insurer's target rating, there are 4 different levels of haircut to the diversification benefit applicable: