SCR Calculator User Manual

Version 1.17 Last modified 2025-4-6

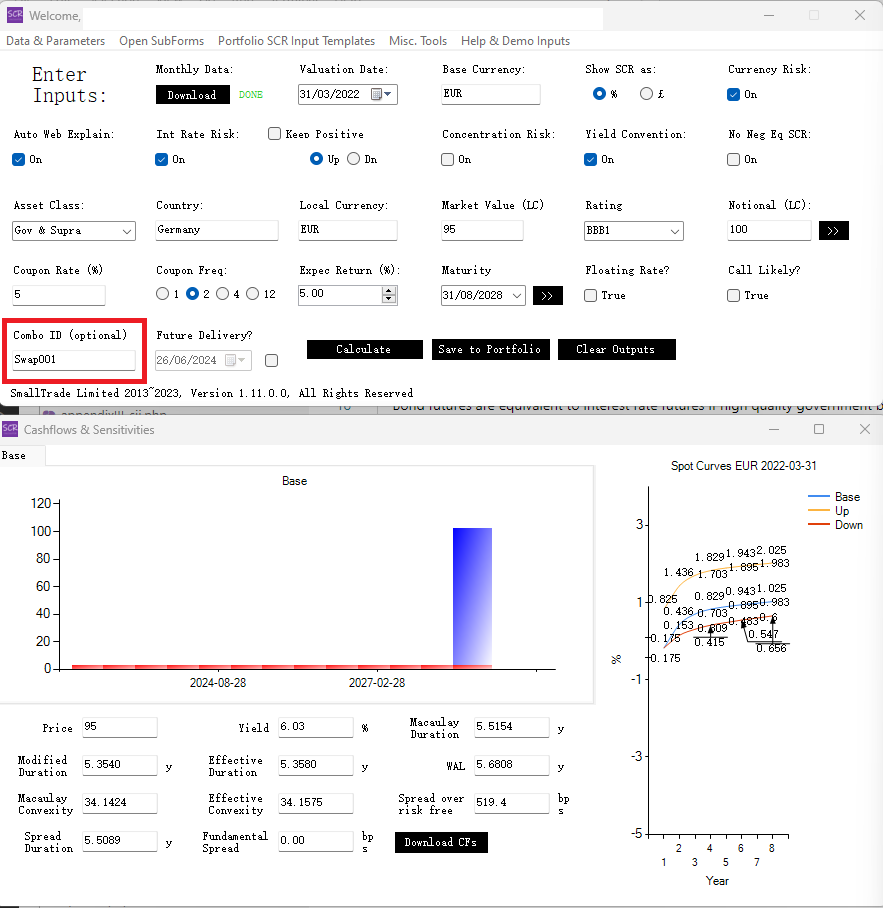

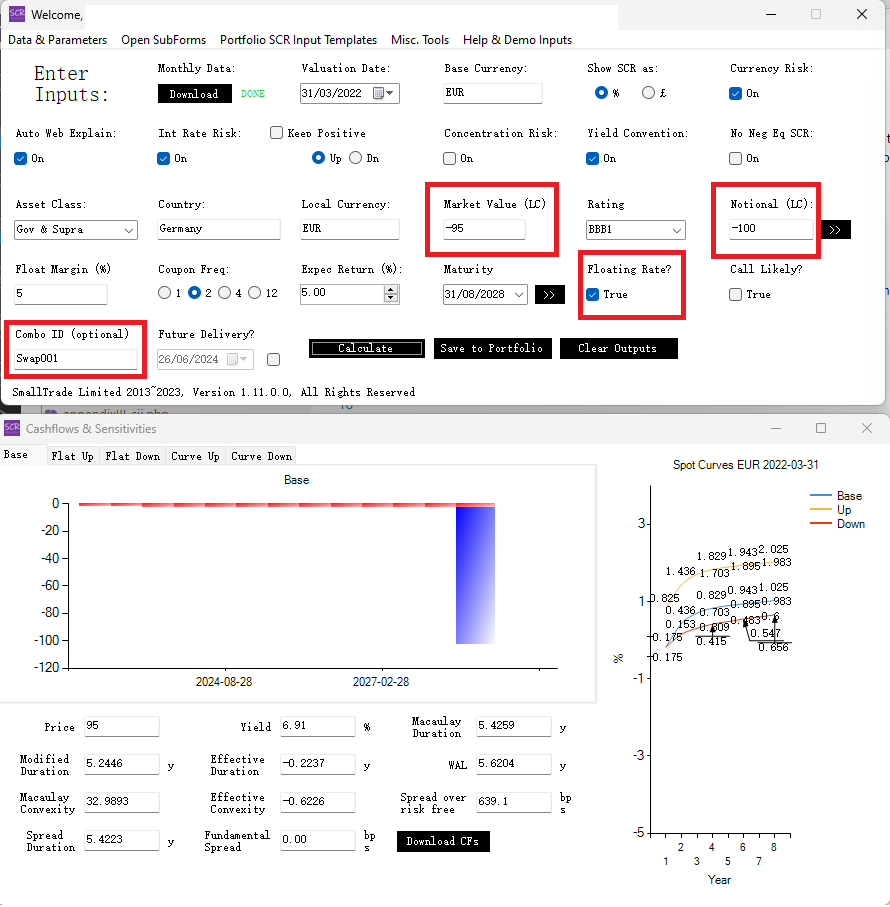

Interest Rate Swaps

The "Combo ID" method allows you to model complex assets easily, such as swaps and convertibles, by grouping related components into a single asset structure.Interest Rate Swaps can be modeled as a "Combo Asset" with two legs: a floating-rate bond and a fixed-rate bond with equal and opposite notionals. In the SCR Calculator, assigning a common "Combo ID" to these two bonds designates them as an interest rate swap.

The Fixed Leg:

The Floating Leg:

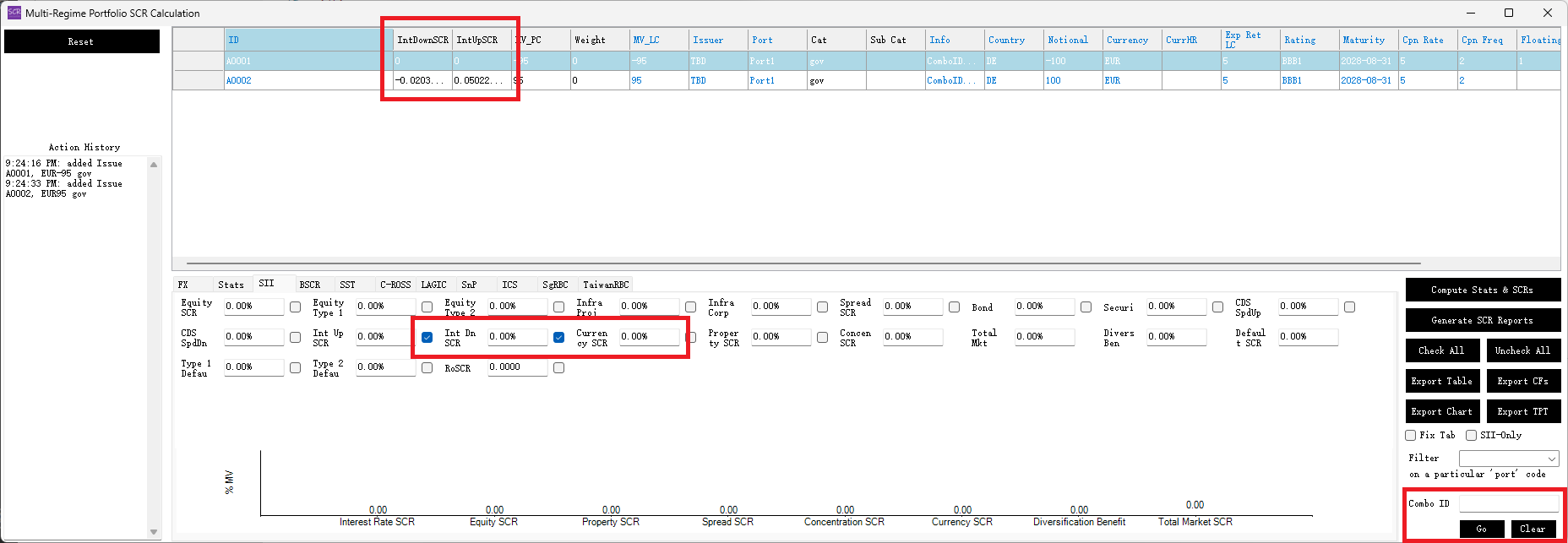

When added to a portfolio with the same Combo ID, the swap's total SCR is shown as zero. However, clicking on individual SCR columns reveals that the fixed-rate leg has interest rate SCRs, while the floating-rate leg does not. Both legs have zero spread SCRs.

When exporting the portfolio, the 'ComboID=xxx;' is automatically added to the 'Info' column of the input sheet. You can also manually add this information directly in the portfolio form or by editing the input sheet.

For large portfolios, use the "Combo ID filter" in the lower-right corner to isolate specific combo assets and review their standalone SCR.

For regular assets, leave the "Combo ID" field empty.