SCR Calculator User Manual

Version 1.17 Last modified 2025-4-6

Overview

The "One-Click" SCR is a convenient button located within the Strategic Asset Allocation form. It is designed for instant Solvency II SCR calculations on a simple allocation table, making it ideal when creating a detailed model portfolio is not required.

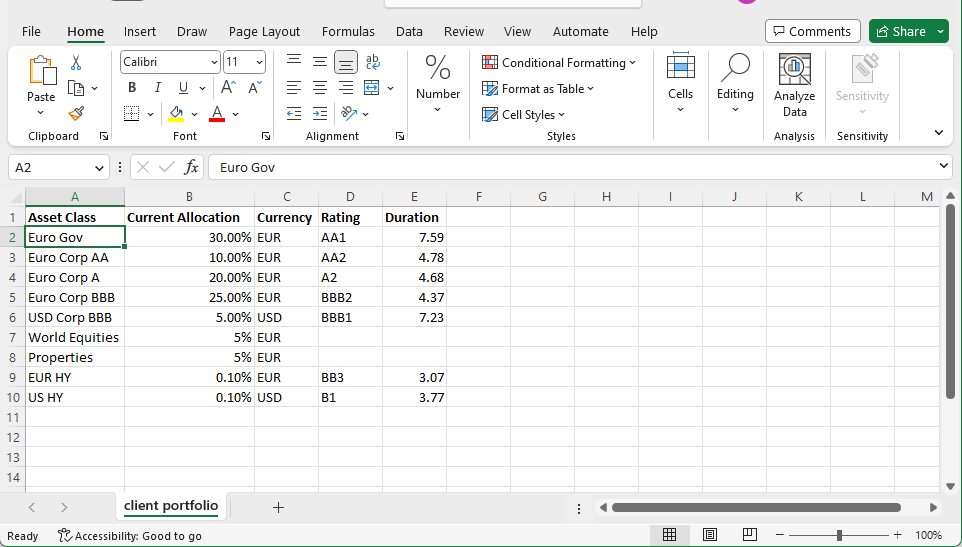

The spreadsheet used in the previous chapter is shown again below. It is a simple allocation table with just five columns, easy enough to construct manually:

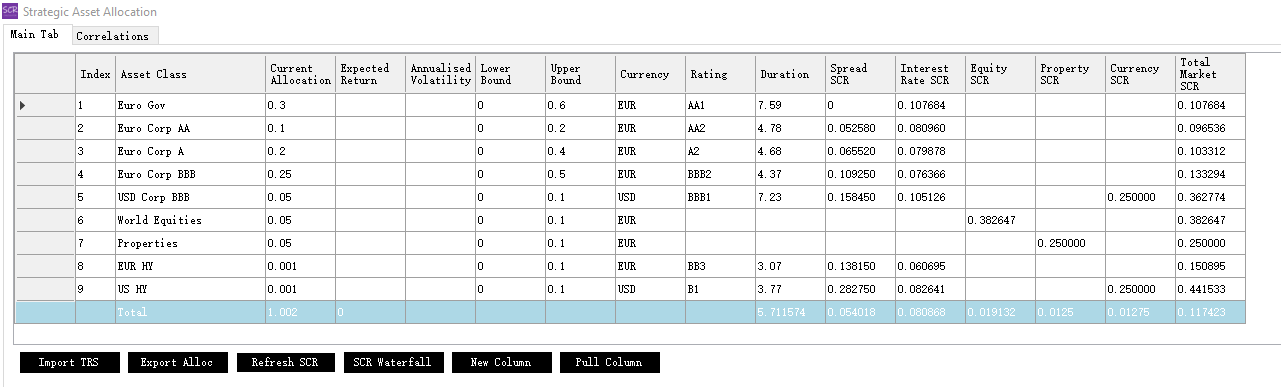

Once imported into the SAA form, pressing the "One-Click SCR" button instantly generates the market risk SCRs as shown below. No additional inputs are required.

If additional columns, such as ESG scores or carbon emission intensities, have been included, they will also appear and can be used as optimization constraints.

The calculator operates by proactively interpreting the meaning and associations of the five input data fields:

- An asset class name containing

"France gov"or"BTP"with non-emptyratinganddurationfields will be identified as a BTP bond by the calculator. - If the asset class name is updated to include a different country name, the calculator will automatically look up the

ratingandcurrencyof the new country in its database and update these fields accordingly. - When the asset class name does not reference government bonds but includes non-empty

ratinganddurationfields, it will be interpreted as a corporate bond. - If no

ratingordurationis provided, but the asset class name contains"property","equity", or a country name, the calculator will interpret the asset as equity issued by or property located in that country. - Asset class names containing

"MBS","ABS","mortgage", etc., will trigger calculations based on the appropriate Solvency II module. - Based on these interpretations, the calculator inserts

SCRcolumns and populates values in the table. - If a

Countrycolumn with 2-letter ISO codes is provided, the calculator will use it to override its default interpretation. - A summary row is added at the end, displaying total allocation weights, weighted

SCRsums, and weighted averages fordurationand other attributes. - The summary row auto-updates whenever the user edits any cell in the table.

- Total market

SCRin the summary row is computed using the proper correlation matrix method. - Users can right-click column headings to delete or rename columns, or use the

"New Column"button to add new ones. If the calculator cannot determine summary stats for the new column, it will prompt the user for input. - If a

"Hedge Ratio"column is present, theFX SCRcolumn values are immediately adjusted to account for those hedge ratios. - After the

"One-Click"button is used, it changes into a"Refresh SCR"button for subsequent updates.

This proactive interpretation is designed to address 90% of SAA scenarios, where asset classes are relatively simple and limited in number, providing fast outcomes with minimal effort.

All values in the allocation table are editable.

Users can manually adjust auto-populated SCR figures if they believe them to be inaccurate. The calculator will respect these manual edits, provided no further changes are made to the corresponding row.

Limitations

- The interest rate SCR calculation in this form is based on a single duration rather than detailed cashflows, which may result in slight differences compared to the more precise calculations available in the "Model Portfolio" form.

- To bypass proactive interpretation, you can use a more generic identifier, such as an ISIN code, as the Asset Class name.