Release Notes

Last Updated: 2024-12-8

9th October 2023

Notch-level Fundamental Spread and Matching Adjustment

The notch-level fundamental spread methodology proposed by the UK PRA is now implemented in the SCR Calculator.

ContextThe UK PRA recently published the CP19/23 public consultation paper as part of the ongoing UK Solvency II Review. The UK version of Solvency II already had slightly-different calibrations of risk-free rates, fundamental spreads and equity symmetric adjustment from EIOPA's since December 2020. Now CP19/23 proposes new, notch-level Matching Adjustment methodology that sets them further apart - although the difference is still small.

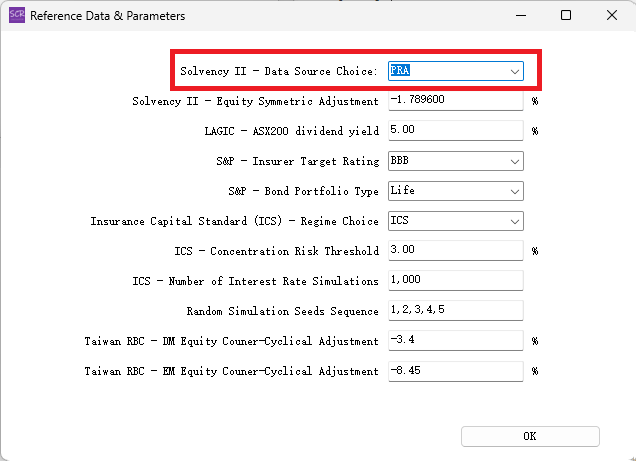

How to Use:From 'Menu' → 'Data & Parameters' → 'Reference Data & Parameters', the user can change the 'Solvency II Data Choice' from 'EIOPA' to 'PRA'. Then click 'OK'.

When 'PRA' is selected, the SCR Calculator will:

- Use the UK PRA's published risk free rates, fundamental spread components (probability of default, cost of downgrade, long-term average spreads) and symmetric adjustments where possible. (These data are stored in the SCR Calculator's database for API use by the programme.) Note, however, that the UK PRA publishes these data on a smaller set of countries than EIOPA does, and also on a later date (usually around the 8th) every month than EIOPA does (usually around the 5th). Where UK PRA data is not available, EIOPA data is used instead.

- Use the UK PRA's notch-level interpolation methodology of the fundamental spread components wherever possible. This methodology is only relevant where it is a corporate or covered bond (not a government bond), and where the bond's rating is not a central notch (e.g. A1 or A3, but not A2), and is not AAA or CCC and below. The SCR Calculator uses the full component interpolation method rather than the other simplified (PD + overall) method. Where notch-level interpolation does occur, it will appear in the explanatory notes of the single asset panel.

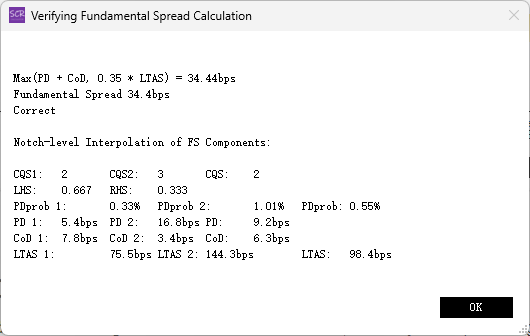

A button is added to the right-hand side of the 'fundamental spread' box in the SCR panel. When the user clicks the button, it gives verification of the fundamental spread calculation, such as below:

- The user can "Get"/"Set" the PD/CoD/FS/LTAS values for all currencies and countries. From 'Menu', select 'Solvency II Matching Adjustment' → 'get', a spreadsheet will be downloaded that contains these sheets: "GovFS", "CorpFS", "CorpPDprob", "CorpPDpct", "CorpCoD", "GovLTAS", "CorpLTASbasic", "CorpLTASoverEURO"; the user can modify these values and/or add rows and then from 'Menu', select 'Solvency II Matching Adjustment' → 'set' to upload the modified spreadsheet. Remember to keep consistency between fundamental spread and long-term average spread.

- PDprob, PDpct, CoD, LTAS, FS, CQS' fields are added in 'MA Potent' checkbox exports in 'Stats' tab in Portfolio SCR Form. These are relevant where the user wishes to investigate or calculate a dynamic MA.

- "ID, PDprob_Better, PDpct_Better, CoD_Better, LTAS_Better, FS_Better, PDprob_Worse, PDpct_Worse, CoD_Worse, LTAS_Worse, FS_Worse" fields are added in 'MA assets' checkbox exports in Portfolio SCR Form. These are relevant where notch-level interpolation took place.

These are further explained in the newly-added Chapter II "Solvency II Matching Adjustment" in the User Manual.

Also, watch the 1-minute trailer below: