Release Notes

Last Updated: 2024-12-8

Taiwan RBC Added in v1.9.0.0

26th July 2023

Taiwan RBC Added in v1.9.0.0

Taiwan RBC is now added in the SCR Calculator.

Old Risk-factor-based RegimeThe current Taiwan RBC regime has been in place since 2004. Taiwan expects to adopt the ICS and IFRS 17 Insurance Contracts in 2026, so there will be two years before we see the back of this older regime.

What are the unique characteristics?Much of the 'uniqueness' is because it is an old regime blended with some new elements from other parts of the world:

- Interest rate risk is calculated based on the spread between insurance contract crediting rate and asset yield, and is very different from ICS and Solvency II.

- Fixed income capital charges are based on notch-level rating.

- Domestic and foreign assets incur different sets of capital charges.

- Domestic ratings are accepted with three-notch-downgrades compared to international Big Three ratings.

- Securitised assets are treated on the same basis as plain bonds.

- Heavier capital treatment on funds than look-through assets: fixed income funds with AA rating will incur a charge similar to a High Yield bond.

- A counter-cyclical symmetric adjustment using the same formula as Solvency II is applied to equity capital charges. The symmetric adjustment is calculated separately for DM and EM equities, and is updated every half year.

- FX capital charges are defined asymmetrically on asset-liability currency-pairs.

- A Herfindahl Index method is used to calculate concentration risk capital on all investment assets apart from cash and government bonds.

- ETFs have their own defined capital charges, because many local insurers tend to trade these funds for short-term profit.

The above points, where relevant, are all reflected in the SCR Calculator's implementation.

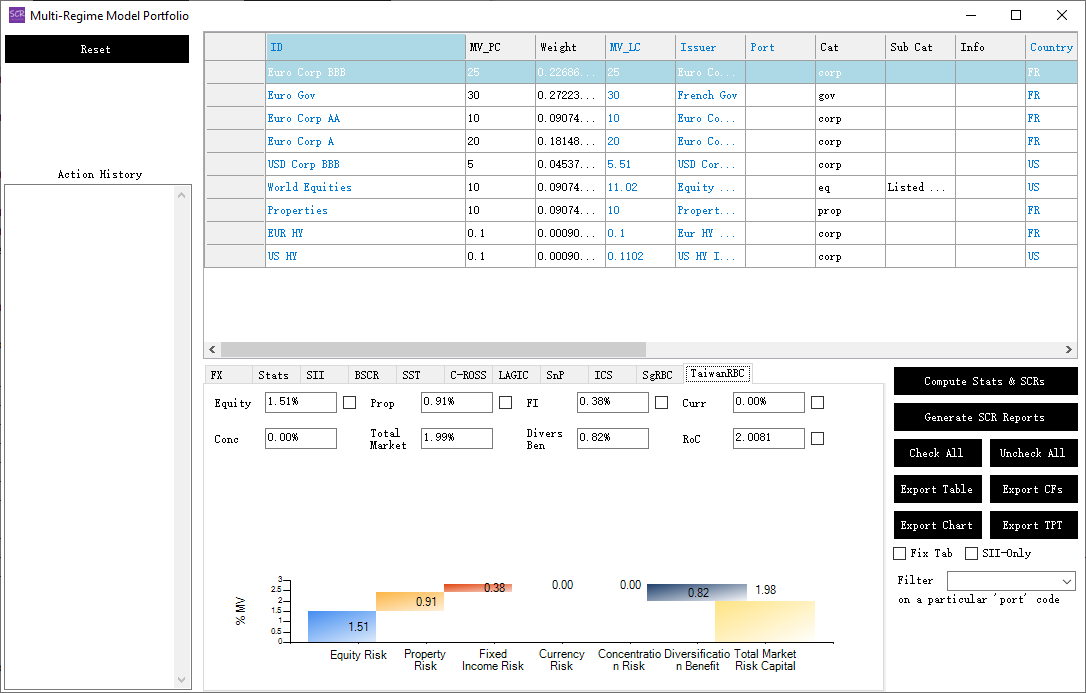

Below is an example screenshot using the SCR Calculator to calculate Taiwan RBC asset charges: