Release Notes

Last Updated: 2024-12-8

2nd June 2024 - New S&P Insurance Capital Regime

2nd June 2024

2nd June 2024 - New S&P Insurance Capital Regime

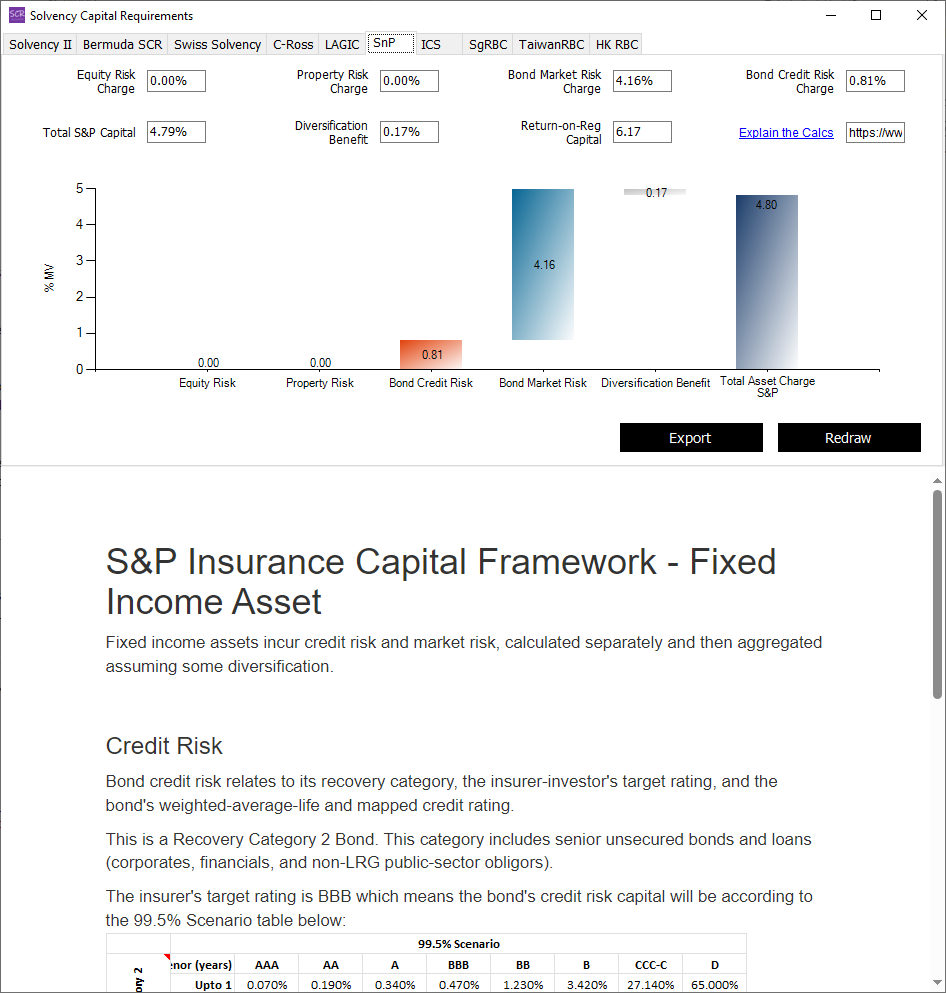

The new S&P Insurance Capital Regime, introduced since November 2023, is now implemented in the SCR Calculator (its asset part):

- The new classification of bonds into four "Recovery Categories" impact how their credit risk capital is calculated. Subordinated and structured credit are affected the most.

- The much-debated differential treatment of assets rated by S&P itself and by other rating agencies was removed, but there are still implications for assets with different country-of-risk origin and BICRA scores.

- Equity and property capital risk groups are re-defined. Infrastructure equity is introduced as a new category, in line with major regulatory regimes.

- Mortgages are subject to a granular classification according to their category, performing status, LTV and DSCR. To reflect these, the DSCR metric is introduced into the SCR Calculator as an additional input.

- Diversification between different market risks, and between market and credit risks, are subject to different correlation assumptions. The haircuts to diversification benefit now vary according to the insurer's target rating.