Release Notes

Last Updated: 2024-12-8

30th April 2023 - S&P Insurance RBC Framework Added

Improvements made in this version (v1.1.2.0)

S&P Insurance Risk Based Capital Frameworkis an important regime especially for general insurers. More details below.- Misc small bug fixes.

S&P highlights from investment point of view:

Ongoing Reform

S&P has been contemplating reforms to its insurance risk-based capital framework for a little while. A new version was proposed in May 2022. The positive changes included more diversification benefit recognised in between asset classes as well as between assets and liabilities; and a recalibration of stresses so they are more unified across different geographical regions, but more granular for asset classes of different nature and seniority. But the proposal faced with strong opposition, including from the US regulator, because of some potentially monopolistic measures, such as downgrading a bond by a notch or two if it was not rated by S&P itself. Now a revised new version, with these questionable clauses removed, is still being discussed.

What we implemented in this release is the current version of the S&P Insurer Capital Framework, which has been in place since July 2010. Once the dust has settled on the new proposal, we will implement the new version.

Comprehensive Assessment

S&P capital is a comprehensive framework that includes both quantitative and qualitative measures. The competitive position, industry & business risk, capital & earnings and funding structure are all taken into consideration, some of which had a subjective judging element. Asset risk charges are only a subset of what led to an insurer's final rating opinion by S&P. However, this part is also the easiest to target and optimise. In my previous shop, I used to look at S&P capital in conjunction with a few other regimes for client balance sheets. The slightly different focus of S&P capital compared to policyholder-focused regulatory regimes had some interesting implications.

Bond, Equity and Property Risk, by Geography

Under the S&P framework, Europe, APAC, Canada and Latin America are unified under the same set of capital charges, while the US has a different set for its life and non-life insurers.

Under all circumstances, asset capital charges depend on the insurer's target rating. For instance, an insurer that targets a BBB rating under S&P would need to post a lot less capital than an insurer that targets a AAA rating.

Equities, properties and bonds incur market risks also depending on the perceived riskiness of their issuing country/location. For bonds, the special point is that an average duration mismatch (by life insurer or general insurer or shareholder fund) of that particular country/market was taken into consideration when S&P calibrated such riskiness. If the insurer is deemed to have sufficient, effective ALM policy in place, such interest-rate related market risk charge can be greatly reduced.

Bonds also incur credit risk, based on their rating and term. They are grouped into different term buckets for such calculation, in a manner less granular than regimes such as Solvency II. Also maybe because of the old age of the current regime, there is little differentiation between assets of different nature and seniority. E.g. a structure note or a mortgage backed security is generally considered more risky than a plain vanilla senior unsecured bond, even though they bear the same official rating. This is being remedied in the upcoming new reform, where fixed income issues are classified into 4 tiers, and structured products are among the lowest tier. But no so in the current framework.

Application

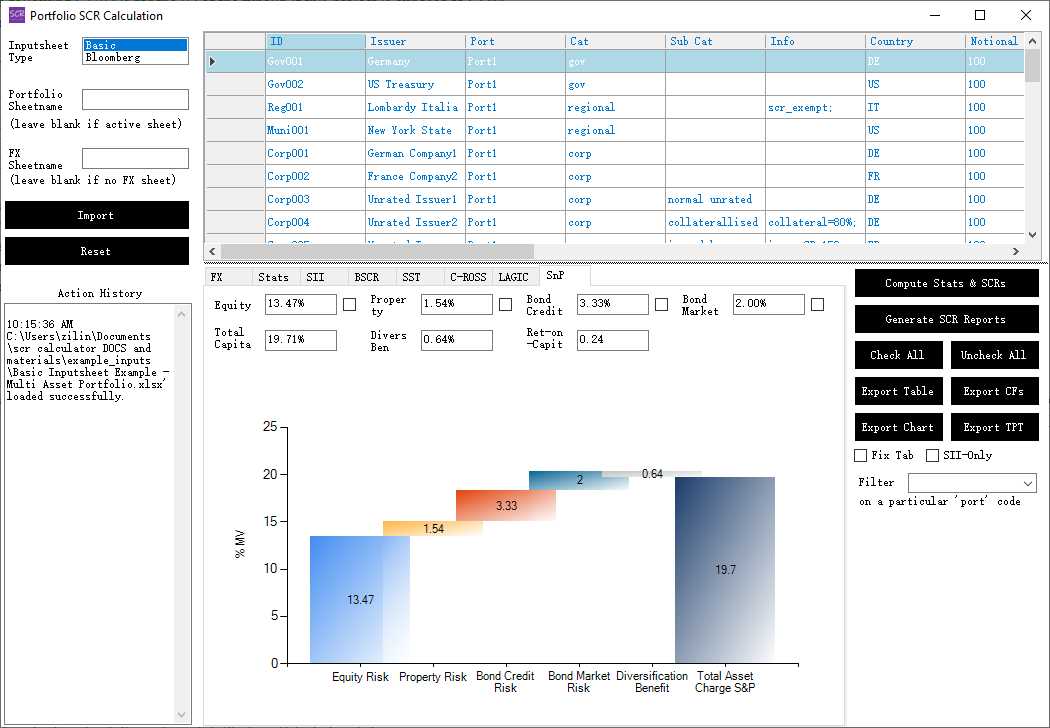

Below is an example screenshot using the SCR Calculator to calculate S&P asset risk charges: