Release Notes

Last Updated: 2024-12-8

17th August 2023

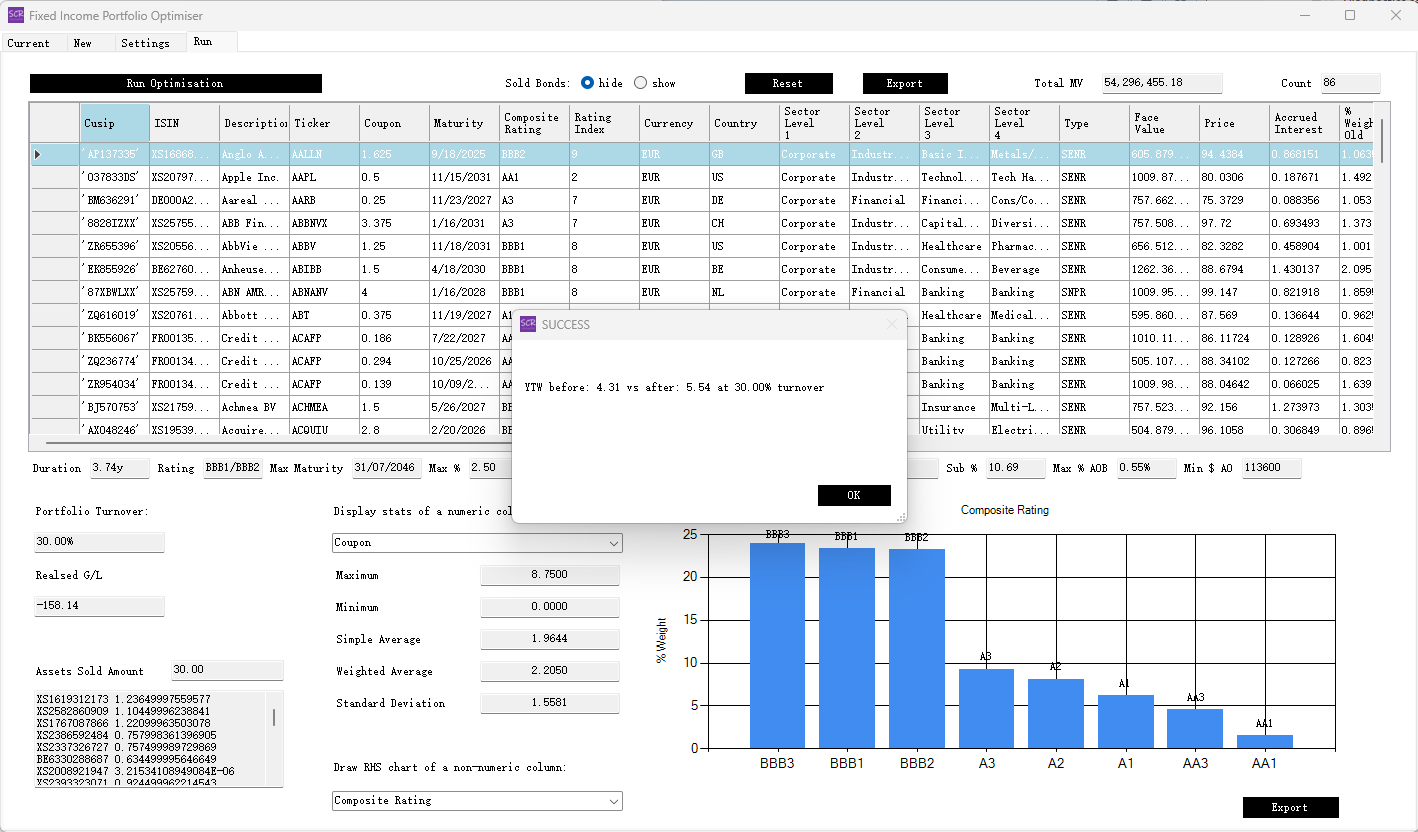

Fixed Income Portfolio Optimiser

Fixed Income Portfolio Optimiser is now added in the SCR Calculator. The Fixed Income Portfolio Optimiser is a unique and versatile portfolio construction tool. Integrated with Bloomberg datafields, it is suitable for improving an existing portfolio at a defined turnover, or building a competitive model portfolio from scratch. By maximising yield or spread while conforming to multi-dimensional constraints, it can generate tangible P&L.

A Powerful Portfolio Construction/Rebalancing ToolQuite often institutional mandates are constructed and maintained under one or several of the following constraints:

- Duration and maturity

- Rating - portfolio average and minimum

- Country and sector exposure limits

- Name and Issue concentration limits

- SCR, multi-jurisdictional

- ESG and other bespoke metrics

- Trading liquidity

- Cashflow needs

The Fixed Income Portfolio Optimiser can make a portfolio manager's life easier. It allows credit fundamentals to be combined with quantitative constraints and can deal with a very large investible universe efficiently. Given proper starting requirements, it can generate fairly practical model portfolios that often beat hand-made ones by several tens of bps or more. These optimised model portfolios can serve as a great starting point for further manual refinement.

Below is an example screenshot: