Release Notes

Last Updated: 2024-12-8

12th June 2023

Improvement and Progress Updates (v1.5.0)

- Insurance Capital Standard v2.0 now in the SCR Calculator.

Important Standard

The Insurance Capital Standard (ICS) is being developed as a consolidated group-wide capital standard for Internationally Active Insurance Groups (IAIGs). ICS v2.0 has entered a monitoring period for confidential reporting since 2019 and detailed technical documents and data collection templates have been published. It is scheduled to become live by Q3 2024. It is now available in the SCR Calculator, among other 6 regimes.

It is a vitally important regime not only for worldwide large insurers, but also for Asia-Pacific countries in particular, as Japan, South-Korea and a few other Asian economies will or have finalised their new economic solvency regimes using the ICS as a template. Insurers in those countries, large or small, will be subject to this new capital regime or a very similar variation of it. The new added ICS regime is designed on a consistent basis with Solvency II, should prove helpful to investment companies ambitious of enhancing their understanding and expanding their local presence in the fast growing Asia-Pacific market.

Technical Features

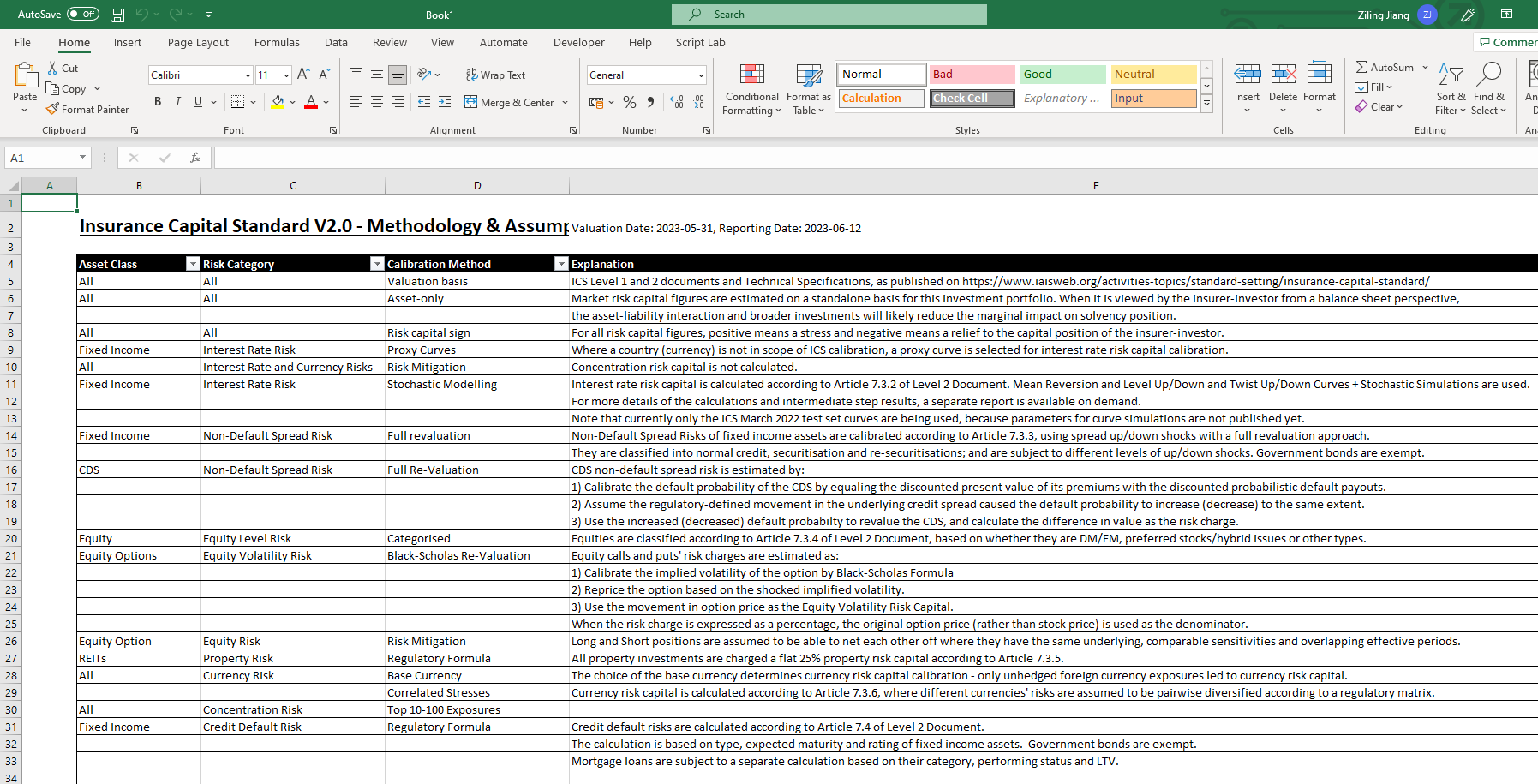

All the market risks - non-default spread, interest rate, equity, property, currency and concentration risks - and credit default risk are implemented.

- The non-default spread module, unlike Solvency II, is based on a full spread stressing approach rather than factors from a rating x duration matrix. Both spread up and spread down stresses are entered into the total market risk aggregation. The default part of spread risk is separately considered in the credit default risk module, making the non-default stresses lighter than otherwise.

- Equity risk includes level and volatility risks. The former is based on a DM/EM/Preferred/Hybrid/Others classification. The latter is based on a tenor-dependent volatility-up stress that affects equity options. Currently there is not a counter-cyclical "symmetric-adjustment" element in it.

- Property risk is a simple 25% stress on all properties.

- Currency risk is applied using a whole balance sheet approach. Currency pairs are first stressed individually based on a regulatory table; then correlated via a uniform 75% correlation assumption. There are 35 currencies currently in scope of the ICS, largely overlapping with the Solvency II risk free curve currencies published by EIOPA.

- Concentration risk is calculated by multiplying the excess exposure of the largest 10-100 counterparties with their equity and credit risk amounts.

- Interest rate risk module is most complex. It is based on calculating the stochastic combination of a set of pre-stressed curves - Mean-Reversion, Level-Up, Level-Down, Twist-Up/Down and Twist-Down/Up - and then taking the VaR of the scenarios.

The interest rate risk module is so far only partially implemented in the calculator. The stochastic simulation part is implemented, but the pre-stressed curves are still those used in the March 2022 fieldtest. This is because pre-stressed curves' stressing parameters are not officially disclosed yet; and any own implementation needs to be based on own calibration - a kind of "reinventing the wheel" that we hadn't done yet but might do in near future.

The SCR Calculator provides a "Curve Overwrite" facility so that confident users can upload their own ICS curve sets for a more precise interest rate risk calibration or stochastic curve generation.

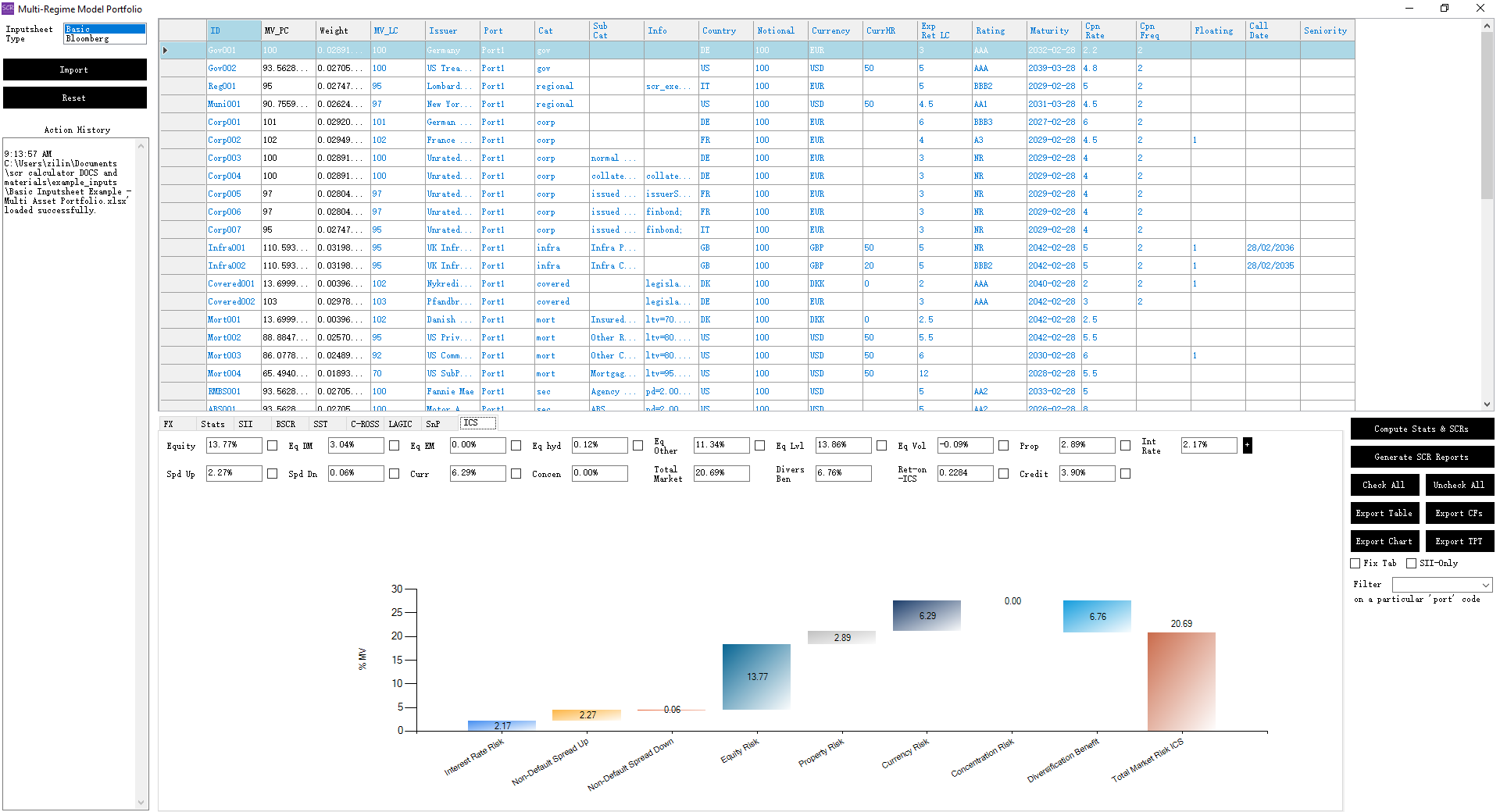

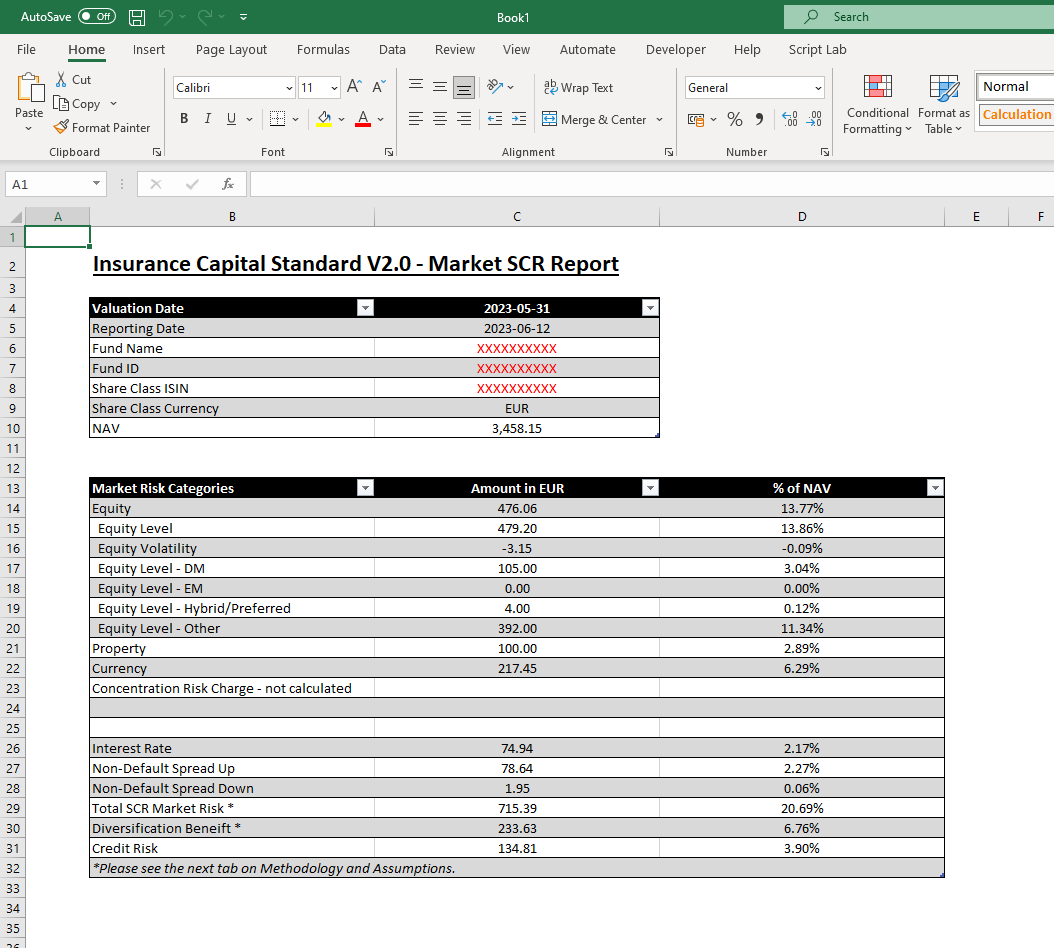

Screenshots