Release Notes

Last Updated: 2024-12-8

24th April 2023 - SII Free; LAGIC Added

Improvements made in this version

- From the v1.1.1.0 release (Monday April 24 2023) onwards, all Solvency II portfolio SCR calculation and reporting functionalities become FREE. Non-Solvency II portfolio SCR calculations are license-based. Single asset SCR calculations under all regimes are still free.

LAGIC, the Australian insurance regime, is added - this is a simple but unique regime. More details below.- Misc small bug fixes.

LAGIC highlights from investment point of view:

- Counter-cyclical growth asset risk charge in a unique way Equity risk charges are applied by adjusting the dividend yield of the ASX200 index up by a certain percentage. Property and infrastructure risk charges are applied in a similar way, but on the individual asset's rental yield. This, using the dividend discount valuation model, leads to a natural counter-cyclical effect on the risk charge.

- Separation of real interest rate movement from inflation movement In most other regimes' standard formula, interest rate risk is calibrated with a single stress. In LAGIC, real interest rate and expected inflation risk are treated as two separate risks. This makes the LAGIC standard formula more similar to typical internal models under Solvency II.

- The Heaviest of Eight Risk Scenarios is Selected 8 combinations of real interest rate up/down, expected inflation up/down and currency up/down are assessed and the heaviest capital result is selected as the final capital charge. This removes some of the problems when a certain risk element is negative, as we typically see under Solvency II.

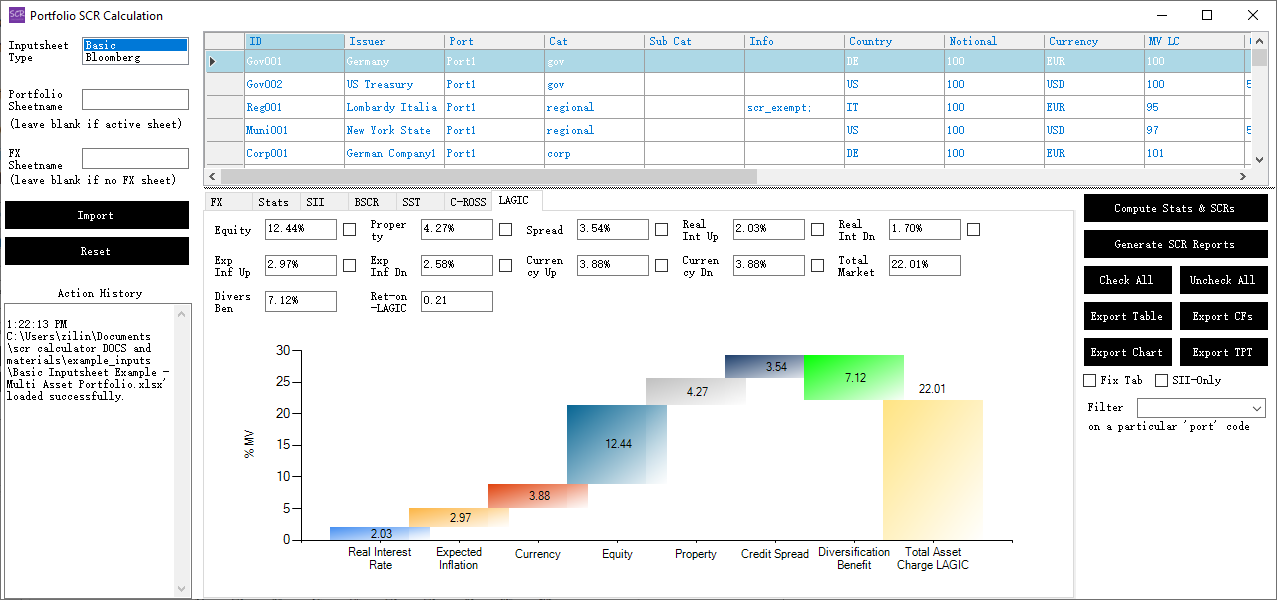

Below is an example screenshot using the SCR Calculator to calculate LAGIC asset charges: